Need it done by 8:30

Q4

Suppose you bought ABC stock at $50 and sold a $54 Call expiring in December for $1. Name the strategy, calculate break-even, max. profit, max. loss and describe the rationale of using the strategy. Draw a graph to help illustrate your answer. Will this strategy be useful to manage risk?

Q5

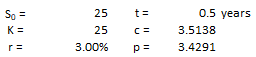

You are given the following data on a European call option and put option for a stock.

Are there any arbitrage opportunities? Carefully explain how you would take advantage of arbitrage opportunities. How much, if any, arbitrage profit can you achieve?

Q6

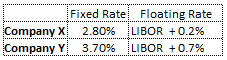

Companies X and Y have been offered the following rates per annum on a $50 million 5-year loan:

Company X requires a floating-rate loan; company Y requires a fixed-rate loan. Design a swap that will net a bank, acting as intermediary, 0.10% per annum and will be equally attractive to X and Y. Draw a graph for your answer.

Q9

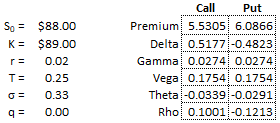

The following data are given for a Stock Option:

a) What is the new call premium if one day passes by and no other changes have occurred?

b) What is the new call premium if volatility decreased from 33% to 32% and there are no other changes?

Q11

As we learned in class, a short strangle is an option strategy with undefined risk.

Identify at least one way of converting this undefined risk to a defined risk strategy. Please explain the pros and cons of your choice

Q12

What is "delta" conceptually and mathematically? Why would we need delta to establish a risk-neutral position? Provide a detailed explanation to get full credit.

Delta is the difference between two values, sometimes it can refer to the rate of change such as in a derivative.

Q13

A U.S. company has accounts receivables in 4 countries: Switzerland (CHF 50M), England (£50M), Germany (€50M) and Italy (€50M). Given the ongoing Covid-19 pandemic and potential repercussions in Europe, where do you see the potential risks going forward? What instruments would you use and how much of the risk would you hedge and in which currency? Give a detailed explanation!