Discussion/ Chapter Summary Chapters 10,11 and 20

Chapter 20- Hybrid Financing: Preferred Stock, Warrants, and Convertibles

Chapter Introduction

The U.S. government’s responses to the global economic crisis were conducted through a wide variety of different programs administered by the Treasury Department, the Federal Reserve, the Federal Deposit Insurance Corporation, and Congress. Each program had a different emphasis, but many of the programs provided cash to troubled companies in exchange for newly issued securities that were (and still are) owned by the U.S. government. In addition to loans, these securities included preferred stock and warrants that are convertible into common stock.

For example, the Treasury bought about in preferred stock from AIG, some of which was later converted to noncumulative preferred stock and common stock. The Treasury bought preferred stock and warrants from hundreds of financial institutions, including Bank of America, Citigroup, and JPMorgan Chase. The Treasury also made loans to GM and Chrysler. Some of the loans were replaced with stock as a part of the automakers’ subsequent bankruptcy settlements.

Two questions arise. First, has the government made profitable investments? No—the government’s daily TARP update estimates that the total lifetime cost of the programs will be about . The U.S. financial system and economy have not (yet) collapsed as badly as they did in the Great Depression, so perhaps the money was well spent.

Second, how much control will the government exert on the companies in which it has invested? Preferred stock does not allow its owners to vote, so the government does not have any direct representation for those investments. The government owns over in the common stock of AIG and GM, but no government employees are on GM’s board.

As you read this chapter, think about the government’s investments in preferred stock and warrants, and decide for yourself whether they were good investments.

Resource

The textbook’s Web site contains an Excelfile that will guide you through the chapter’s calculations. The file for this chapter is Ch20 Tool Kit.xls, and we encourage you to open the file and follow along as you read the chapter.

In previous chapters, we examined common stocks and various types of long-term debt. In this chapter, we examine three other securities used to raise long-term capital:

(1)

preferred stock, which is a hybrid security that represents a cross between debt and common equity,

(2)

warrants, which are derivative securities issued by firms to facilitate the issuance of some other type of security, and

(3)

convertibles, which combine the features of debt (or preferred stock) and warrants.

Preferred stock is a hybrid—it is similar to bonds in some respects and to common stock in other ways. Accountants classify preferred stock as equity; hence they show it on the balance sheet as an equity account. However, from a financial perspective preferred stock lies somewhere between debt and common equity: It imposes a fixed charge and thus increases the firm’s financial leverage, yet omitting the preferred dividend does not force a company into bankruptcy. Also, unlike interest on debt, preferred dividends are not deductible by the issuing corporation, so preferred stock has a higher cost of capital than does debt. We first describe the basic features of preferred stock, after which we discuss the types of preferred stock and the advantages and disadvantages of preferred stock.

20-1a

Basic Features

Preferred stock has a par (or liquidating) value, often either or . The dividend is stated as either a percentage of par, as so many dollars per share, or both ways. For example, several years ago Klondike Paper Company sold shares of par value perpetual preferred stock for a total of . This preferred stock had a stated annual dividend of per share, so the preferred dividend yield was , or , at the time of issue. The dividend was set when the stock was issued; it will not be changed in the future. Therefore, if the required rate of return on preferred, , changes from after the issue date—as it did—then the market price of the preferred stock will go up or down. Currently, for Klondike Paper’s preferred is , and the price of the preferred has risen from to .

If the preferred dividend is not earned, the company does not have to pay it. However, most preferred issues are cumulative, meaning that the cumulative total of unpaid preferred dividends must be paid before dividends can be paid on the common stock. Unpaid preferred dividends are called arrearages. Dividends in arrears do not earn interest; thus, arrearages do not grow in a compound interest sense, they only grow from additional nonpayments of the preferred dividend. Also, many preferred stocks accrue arrearages for only a limited number of years—so that, for example, the cumulative feature may cease after . However, the dividends in arrears continue in force until they are paid.

Preferred stock normally has no voting rights. However, most preferred issues stipulate that the preferred stockholders can elect a minority of the directors—say, three out of ten—if the preferred dividend is passed (omitted). Some preferreds even entitle their holders to elect a majority of the board.

Although nonpayment of preferred dividends will not trigger bankruptcy, corporations issue preferred stock with every intention of paying the dividend. Even if passing the dividend does not give the preferred stockholders control of the company, failure to pay a preferred dividend precludes payment of common dividends. In addition, passing the dividend makes it difficult to raise capital by selling bonds and virtually impossible to sell more preferred or common stock except at rock-bottom prices. However, having preferred stock outstanding does give a firm the chance to overcome its difficulties: If bonds had been used instead of preferred stock, a company could be forced into bankruptcy before it could straighten out its problems. Thus, from the viewpoint of the issuing corporation, preferred stock is less risky than bonds.

The Romance Had No Chemistry, but it Had a Lot of Preferred Stock!

On April 1, 2009, Dow Chemical Company merged with Rohm & Haas after a bitter dispute over the interpretation of their previous merger agreement. So even though the two companies make chemicals, there apparently wasn’t much chemistry by the time the merger was completed.

To raise cash for the per share purchase of Rohm & Haas’s outstanding shares, Dow borrowed over from Citibank and also issued in convertible preferred stock to Berkshire Hathaway and The Kuwait Investment Authority.

The Haas Family Trusts and Paulson & Company were large shareholders in Rohm & Haas. As part of the deal, they sold their shares to Dow with one hand and bought in preferred stock from Dow with the other. This preferred stock pays a cash dividend of . It also pays an “dividend” that either can be cash or additional shares of the preferred stock, with the choice left to Dow; this is called a payment-in-kind (PIK) dividend.

These terms mean that Dow can conserve cash if it runs into difficult times: Dow can pay the in additional stock and Dow can even defer payment of the cash dividend without risk of bankruptcy. But if this happens, a troubled marriage is likely to cause even more grief.

Source: 8-K reports from the SEC filed on March 12, 2009 and April 1, 2009.

WWW

For updates, go to http://finance.yahoo.com and get quotes for AA-P, Alcoa’s preferred stock. For an updated bond yield, use the bond screener and search for Alcoa bonds.

For an investor, however, preferred stock is riskier than bonds:

(1) preferred stockholders’ claims are subordinated to those of bondholders in the event of liquidation, and

(2) bondholders are more likely to continue receiving income during hard times than are preferred stockholders.

Accordingly, investors require a higher after-tax rate of return on a given firm’s preferred stock than on its bonds. However, because of preferred dividends is exempt from corporate taxes, preferred stock is attractive to corporate investors. Indeed, high-grade preferred stock, on average, sells on a lower pre-tax yield basis than high-grade bonds. As an example, Alcoa has preferred stock with an annual dividend of (a rate applied to par value). In June 2012, Alcoa’s preferred stock had a price of , for a market yield of about . Alcoa’s long-term bonds that mature in 2037 provided a yield of , which is points more than its preferred, even though preferred stock is riskier than debt. The tax treatment accounted for this differential; the after-tax yield to corporate investors was greater on the preferred stock than on the bonds because of the dividend may be excluded from taxation by a corporate investor.![]()

About half of all preferred stock issued in recent years has been convertible into common stock. We discuss convertibles in Section 20-3.

Some preferred stocks are similar to perpetual bonds in that they have no maturity date, but most new issues now have specified maturities. For example, many preferred shares have a sinking fund provision that calls for the retirement of of the issue each year, meaning the issue will “mature” in a maximum of . Also, many preferred issues are callable by the issuing corporation, which can also limit the life of the preferred.![]()

Nonconvertible preferred stock is virtually all owned by corporations, which can take advantage of the dividend exclusion to obtain a higher after-tax yield on preferred stock than on bonds. Individuals should not own preferred stocks (except convertible preferreds)—they can get higher yields on safer bonds, so it is not logical for them to hold preferreds.![]() As a result of this ownership pattern, the volume of preferred stock financing is geared to the supply of money in the hands of corporate investors. When the supply of such money is plentiful, the prices of preferred stocks are bid up, their yields fall, and investment bankers suggest that companies in need of financing consider issuing preferred stock.

As a result of this ownership pattern, the volume of preferred stock financing is geared to the supply of money in the hands of corporate investors. When the supply of such money is plentiful, the prices of preferred stocks are bid up, their yields fall, and investment bankers suggest that companies in need of financing consider issuing preferred stock.

For issuers, preferred stock has a tax disadvantage relative to debt: Interest expense is deductible, but preferred dividends are not. Still, firms with low tax rates may have an incentive to issue preferred stock that can be bought by high-tax-rate corporate investors, who can take advantage of the dividend exclusion. If a firm has a lower tax rate than potential corporate buyers, then the firm might be better off issuing preferred stock than debt. The key here is that the tax advantage to a high-tax-rate corporation is greater than the tax disadvantage to a low-tax-rate issuer. As an illustration, assume that risk differentials between debt and preferred would require an issuer to set the interest rate on new debt at and the dividend yield on new preferred stock higher, or at in a no-tax world. However, when taxes are considered, a corporate buyer with a high tax rate—say, —might be willing to buy the preferred stock if it has an before-tax yield. This would produce an after-tax return on the preferred versus on the debt. If the issuer has a low tax rate—say, —then its after-tax costs would be on the bonds and on the preferred. Thus, the security with lower risk to the issuer, preferred stock, also has a lower cost. Such situations can make preferred stock a logical financing choice.![]()

Hybrids Aren’t Only for Corporations

The Cooperative Regions of Organic Producer Pools (CROPP) markets organic produce under such brand names as Organic Valley and Organic Prairie and is a supplier to Stonyfield, maker of organic yogurt. CROPP is not a corporation or a partnership. It is a cooperative, which is an organization that provides services for its owner/members. In this case, CROPP purchases produce from its members, processes the produce, and then resells it. Profits are redistributed to the owner/members as dividends.

With the beginnings of the financial recovery and an overall increase in the demand for organic products, CROPP’s sales grew in 2009 to over . High growth requires investments in operating assets, causing CROPP to need in additional external financing. CROPP decided to raise the funds by issuing preferred stock to members and non-members. CROPP had successfully issued preferred stock in the past and this issue was a par, cumulative dividend, non-voting preferred stock, and was sold for per share. CROPP chose not to use an investment banker for this issue; the co-op’s investor relations manager was in charge of marketing and selling the preferred stock and CROPP saved quite a bit of money in fees with issuance costs totaling about rather than the or more charged by an investment bank.

Unlike preferred stock issued by corporations, dividends on preferred stock issued by a Section 521 cooperative such as CROPP can be deducted from its pretax income, and the dividend recipient treats it as ordinary income for tax purposes. Therefore this preferred stock is treated like perpetual debt for tax purposes. Why then would CROPP issue preferred stock rather than debt? The simple reason is that preferred stock is non-recourse. If CROPP misses a dividend payment, the dividend accrues, but the preferred stockholder cannot force CROPP into bankruptcy. This flexibility is valuable, especially in an industry as volatile as farming.

20-1b

Other Types of Preferred Stock

In addition to “plain vanilla” preferred stock, there are two other variations: adjustable rate and market auction preferred stock.

Adjustable Rate Preferred Stock

Instead of paying fixed dividends, adjustable rate preferred stock (ARP) has dividends tied to the rate on Treasury securities. ARPs are issued mainly by utilities and large commercial banks. When ARPs were first developed, they were touted as nearly perfect short-term corporate investments because

(1) only of the dividends are taxable to corporations, and

(2) the floating-rate feature was supposed to keep the issue trading at near par.

The new security proved to be popular as a short-term investment for firms with idle cash, so mutual funds that held ARPs sprouted like weeds (and shares of these funds, in turn, were purchased by corporations). However, the ARPs still had some price volatility due to

(1) changes in the riskiness of the issuers (some big banks that had issued ARPs, such as Continental Illinois, ran into serious loan default problems) and

(2) fluctuations in Treasury yields between dividend rate adjustment dates.

Therefore, the ARPs had too much price instability to be held in the liquid asset portfolios of many corporate investors.

Market Auction Preferred Stock

In 1984, investment bankers introduced money market preferred stock, which is also called market auction preferred stock.![]() Here the underwriter conducts an auction on the issue every . (To get the exclusion from taxable income, buyers must hold the stock for at least .) Holders who want to sell their shares can put them up for auction at par value. Buyers then submit bids in the form of the yields they are willing to accept over the next period. The yield set on the issue for the coming period is the lowest yield sufficient to sell all the shares being offered at that auction. The buyers pay the sellers the par value; hence holders are virtually assured that their shares can be sold at par. The issuer then must pay a dividend rate over the next period as determined by the auction. From the holder’s standpoint, market auction preferred is a low-risk, largely tax-exempt, maturity security that can be sold between auction dates at close to par.

Here the underwriter conducts an auction on the issue every . (To get the exclusion from taxable income, buyers must hold the stock for at least .) Holders who want to sell their shares can put them up for auction at par value. Buyers then submit bids in the form of the yields they are willing to accept over the next period. The yield set on the issue for the coming period is the lowest yield sufficient to sell all the shares being offered at that auction. The buyers pay the sellers the par value; hence holders are virtually assured that their shares can be sold at par. The issuer then must pay a dividend rate over the next period as determined by the auction. From the holder’s standpoint, market auction preferred is a low-risk, largely tax-exempt, maturity security that can be sold between auction dates at close to par.

In practice, things may not go quite so smoothly. If there are few potential buyers, then an excessively high yield might be required to clear the market. To protect the issuing firms or mutual funds from high dividend payments, the securities have a cap on the allowable dividend yield. If the market-clearing yield is higher than this cap, then the next dividend yield will be set equal to this cap rate, but the auction will fail and the owners of the securities who wish to sell will not be able to do so. This happened in February 2008, and many market auction preferred stockholders were left holding securities they wanted to liquidate.

There are both advantages and disadvantages to financing with preferred stock. Here are the major advantages from the issuer’s standpoint.

In contrast to bonds, the obligation to pay preferred dividends is not firm, and passing (not paying) a preferred dividend cannot force a firm into bankruptcy.

By issuing preferred stock, the firm avoids the dilution of common equity that occurs when common stock is sold.

Because preferred stock sometimes has no maturity and because preferred sinking fund payments (if present) are typically spread over a long period, preferred issues reduce the cash flow drain from repayment of principal that occurs with debt issues.

There are two major disadvantages, as follows.

Preferred stock dividends are not normally deductible to the issuer, so the after-tax cost of preferred is typically higher than the after-tax cost of debt. However, the tax advantage of preferreds to corporate purchasers lowers its pre-tax cost and thus its effective cost.

Although preferred dividends can be passed, investors expect them to be paid and firms intend to pay them if conditions permit. Thus, preferred dividends are considered to be a fixed cost. As a result, their use—like that of debt—increases financial risk and hence the cost of common equity.

A warrant is a certificate issued by a company that gives the holder the right to buy a stated number of shares of the company’s stock at a specified price for some specified length of time. Generally, warrants are issued along with debt, and they are used to induce investors to buy long-term debt with a lower coupon rate than would otherwise be required. For example, when Infomatics Corporation, a rapidly growing high-tech company, wanted to sell of bonds in 2013, the company’s investment bankers informed the financial vice president that the bonds would be difficult to sell and that a coupon rate of would be required. However, as an alternative the bankers suggested that investors might be willing to buy the bonds with a coupon rate of only if the company would offer warrants with each bond, each warrant entitling the holder to buy one share of common stock at a strike price (also called an exercise price) of per share. The stock was selling for per share at the time, and the warrants would expire in the year 2023 if they had not been exercised previously.

Why would investors be willing to buy Infomatics’s bonds at a yield of only in a market just because warrants were also offered as part of the package? It’s because the warrants are long-term call options that allow holders to buy the firm’s common stock at the strike price regardless of how high the market price climbs. The value of this option offsets the low interest rate on the bonds and makes the package of low-yield bonds plus warrants attractive to investors. (See Chapter 8 for a discussion of options.)

20-2a

Initial Market Price of a Bond with Warrants

If the Infomatics bonds had been issued as straight debt, they would have carried a interest rate. However, with warrants attached, the bonds were sold to yield . Someone buying the bonds at their initial offering price would thus be receiving a package consisting of an , bond plus warrants. Because the going interest rate on bonds as risky as those of Infomatics was , we can find the straight-debt value of the bonds, assuming an annual coupon for ease of illustration, as follows:

Using a financial calculator, input , , , and . Then press the key to obtain the bond’s value of , or approximately . Thus, a person buying the bonds in the initial underwriting would pay and receive in exchange a straight bond worth about plus warrants that are presumably worth about :

(20-1)

Because investors receive warrants with each bond, each warrant has an implied value of .

The key issue in setting the terms of a bond-with-warrants deal is valuing the warrants. The straight-debt value can be estimated quite accurately, as we have shown. However, it is more difficult to estimate the value of the warrants. The Black-Scholes option pricing model (OPM), discussed in Chapter 8, can be used to find the value of a call option. There is a temptation to use this model to find the value of a warrant, because call options are similar to warrants in many respects: Both give the investor the right to buy a share of stock at a fixed strike price on or before the expiration date. However, there are major differences between call options and warrants. When call options are exercised, the stock provided to the option holder comes from the secondary market, but when warrants are exercised, the stock provided to the warrant holders is either newly issued shares or treasury stock the company has previously purchased. This means that the exercise of warrants dilutes the value of the original equity, which could cause the value of the original warrant to differ from the value of a similar call option. Also, call options typically have a life of just a few months, whereas warrants often have lives of or more. Finally, the Black-Scholes model assumes that the underlying stock pays no dividend, which is not unreasonable over a short period but is unreasonable for or . Therefore, investment bankers cannot use the original Black-Scholes model to determine the value of warrants.

Even though the original Black-Scholes model cannot be used to determine a precise value for a warrant, there are more sophisticated models that work reasonably well.![]() In addition, investment bankers can simply contact portfolio managers of mutual funds, pension funds, and other organizations that would be interested in buying the securities to get an indication of how many they would buy at different prices. In effect, the bankers hold a presale auction and determine the set of terms that will just clear the market. If they do this job properly then they will, in effect, be letting the market determine the value of the warrants.

In addition, investment bankers can simply contact portfolio managers of mutual funds, pension funds, and other organizations that would be interested in buying the securities to get an indication of how many they would buy at different prices. In effect, the bankers hold a presale auction and determine the set of terms that will just clear the market. If they do this job properly then they will, in effect, be letting the market determine the value of the warrants.

Warrants generally are used by small, rapidly growing firms as sweeteners when they sell debt or preferred stock. Such firms frequently are regarded by investors as being highly risky, so their bonds can be sold only at extremely high coupon rates and with very restrictive indenture provisions. To avoid such restrictions, firms like Infomatics often offer warrants along with the bonds.

Getting warrants along with bonds enables investors to share in the company’s growth, assuming it does in fact grow and prosper. Therefore, investors are willing to accept a lower interest rate and less restrictive indenture provisions. A bond with warrants has some characteristics of debt and some characteristics of equity. It is a hybrid security that provides the financial manager with an opportunity to expand the firm’s mix of securities and thereby appeal to a broader group of investors.

Virtually all warrants issued today are detachable. In other words, after a bond with attached warrants is sold, the warrants can be detached and traded separately from the bond. Further, even after the warrants have been exercised, the bond (with its low coupon rate) remains outstanding.

The strike price on warrants is generally set some to above the market price of the stock on the date the bond is issued. If the firm grows and prospers, causing its stock price to rise above the strike price at which shares may be purchased, warrant holders could exercise their warrants and buy stock at the stated price. However, without some incentive, warrants would never be exercised prior to maturity—their value in the open market would be greater than their value if exercised, so holders would sell warrants rather than exercise them. There are three conditions that cause holders to exercise their warrants:

(1)

Warrant holders will surely exercise and buy stock if the warrants are about to expire and the market price of the stock is above the exercise price.

(2)

Warrant holders will exercise voluntarily if the company raises the dividend on the common stock by a sufficient amount. No dividend is earned on the warrant, so it provides no current income. However, if the common stock pays a high dividend, then it provides an attractive dividend yield but limits stock price growth. This induces warrant holders to exercise their option to buy the stock.

(3)

Warrants sometimes have stepped-up strike prices (also called stepped-up exercise prices), which prod owners into exercising them.

For example, Williamson Scientific Company has warrants outstanding with a strike price of until December 31, 2016, at which time the strike price rises to . If the price of the common stock is over just before December 31, 2016, many warrant holders will exercise their options before the stepped-up price takes effect and the value of the warrants falls.

Another desirable feature of warrants is that they generally bring in funds only if funds are needed. If the company grows, it will probably need new equity capital. At the same time, growth will cause the price of the stock to rise and the warrants to be exercised; hence the firm will obtain the cash it needs. If the company is not successful and it cannot profitably employ additional money, then the price of its stock will probably not rise enough to induce exercise of the warrants.

20-2c

The Component Cost of Bonds with Warrants

When Infomatics issued its bonds with warrants, the firm received for each bond. The pre-tax cost of debt would have been if no warrants had been attached, but each Infomatics bond has warrants, each of which entitles its holder to buy one share of stock for . The presence of warrants also allows Infomatics to pay only interest on the bonds, obligating it to pay interest for plus at the end of . What is the percentage cost of each bond with warrants? As we shall see, the cost is well above the coupon rate on the bonds.

The best way to approach this analysis is to break the into two components, one consisting of an bond and the other consisting of of warrants. Thus, the bond-with-warrants package consists of straight debt and warrant. Our objective is to find the cost of capital for the straight bonds and the cost of capital for the warrant, and then weight them to derive the cost of capital for the bond-with-warrants package.

The pre-tax cost of debt is because this is the pre-tax cost of debt for a straight bond, so our task is to estimate the cost of capital for a warrant. Estimating the cost of capital for a warrant is fairly complicated, but we can use the following procedure to obtain a reasonable approximation.![]() The basic idea is to estimate the firm’s expected cost of satisfying the warrant holders at the time the warrants expire. To do this, we need to estimate the value the firm, the value of the debt, the intrinsic value of equity, and the stock price at the time of expiration.

The basic idea is to estimate the firm’s expected cost of satisfying the warrant holders at the time the warrants expire. To do this, we need to estimate the value the firm, the value of the debt, the intrinsic value of equity, and the stock price at the time of expiration.

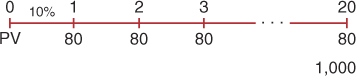

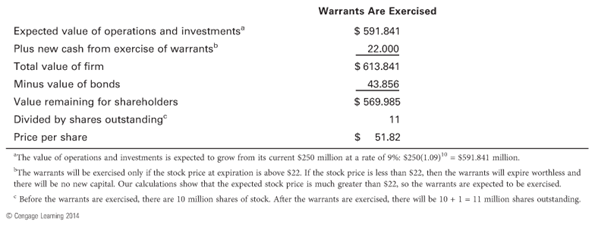

Assume that the total value of Infomatics’s operations and investments, which is immediately after issuing the bonds with warrants, is expected to grow at . When the warrants are due to expire in , the total value of Infomatics is expected to be .

Infomatics will receive per warrant when exercised; with warrants, this creates a cash flow to Infomatics. The total value of Infomatics will be equal to the value of operations plus the value of this cash. This will make the total value of Infomatics equal to .

When the warrants expire, the bonds will have remaining until maturity with a fixed coupon payment of . If the expected market interest rate is still , then the time line of cash flows will be

Using a financial calculator, input , , , and ; then press the key to obtain the bond’s value, . The total value of all of the bonds is .

The intrinsic value of equity is equal to the total value of the firm minus the value of debt: .

Infomatics had shares outstanding prior to the warrants’ exercise, so it will have after the options are exercised. The previous warrant holders will now own of the equity, for a total of . We can also estimate the predicted intrinsic stock price, which is equal to the intrinsic value of equity divided by the number of shares: per share.![]() These calculations are summarized in Table 20-1.

These calculations are summarized in Table 20-1.

Table 20-1

Valuation Analysis after Exercise of Warrants in (Millions of Dollars, Except for Per Share Data)

![]()

To find the component cost of the warrants, consider that Infomatics will have to issue one share of stock worth for each warrant exercised and, in return, Infomatics will receive the strike price, . Thus, a purchaser of the bonds with warrants, if she holds the complete package, would expect to realize a profit in Year of for each warrant exercised.![]() Because each bond has warrants attached and because each warrant entitles the holder to buy one share of common stock, it follows that warrant holders will have an expected cash flow of per bond at the end of Year . Here is a time line of the expected cash flow stream to a warrant holder:

Because each bond has warrants attached and because each warrant entitles the holder to buy one share of common stock, it follows that warrant holders will have an expected cash flow of per bond at the end of Year . Here is a time line of the expected cash flow stream to a warrant holder:

![]()

The IRR of this stream is , which is an approximation of the warrant holder’s expected return on the warrants ( ) in the bond with warrants. The overall pre-tax cost of capital for the bonds with warrants is the weighted average of the cost of straight debt and the cost of warrants:

![]()

The cost of the warrants is higher than the cost of debt because warrants are riskier than debt; in fact, the cost of warrants is greater than the cost of equity because warrants also are riskier than equity. Thus, the cost of capital for a bond with warrants is weighted between the cost of debt and the much higher cost of equity. This means the overall cost of capital for the bonds with warrants will be greater than the cost of straight debt and will be much higher than the coupon rate on the bonds-with-warrants package.![]()

Bonds with warrants and preferred stock with warrants have become an important source of funding for companies during the global economic crisis. But as our example shows, this form of financing has a much higher cost of capital than its low coupon and preferred dividend might lead you to think.![]()

Convertible securities are bonds or preferred stocks that, under specified terms and conditions, can be exchanged for (that is, converted into) common stock at the option of the holder. Unlike the exercise of warrants, which brings in additional funds to the firm, conversion does not provide new capital; debt (or preferred stock) is simply replaced on the balance sheet by common stock. Of course, reducing the debt or preferred stock will improve the firm’s financial strength and make it easier to raise additional capital, but that requires a separate action.

20-3a

Conversion Ratio and Conversion Price

Resource

See Ch20 Tool Kit.xls on the textbook’s Web site for details.

The conversion ratio, CR, for a convertible security is defined as the number of shares of stock a bondholder will receive upon conversion. The conversion price, , is defined as the effective price investors pay for the common stock when conversion occurs. The relationship between the conversion ratio and the conversion price can be illustrated by Silicon Valley Software Company’s convertible debentures issued at their par value in July of 2013. At any time prior to maturity on July 15, 2033, a debenture holder can exchange a bond for shares of common stock. Therefore, the conversion ratio, , is . The bond cost a purchaser , the par value, when it was issued. Dividing the par value by the shares received gives a conversion price of a share:

(20-2)

Conversely, by solving for , we obtain the conversion ratio:

(20-3)

Once is set, the value of is established, and vice versa.

Like a warrant’s exercise price, the conversion price is typically set some to above the prevailing market price of the common stock on the issue date. Generally, the conversion price and conversion ratio are fixed for the life of the bond, with the exception of protection against dilutive actions the company might take, including stock splits, stock dividends, and the sale of common stock at prices below the conversion price.![]()

The typical protective provision states that if the stock is split or if a stock dividend is declared, the conversion price must be lowered by the percentage amount of the stock dividend or split. For example, if Silicon Valley Software (SVS) were to have a -for- stock split, then the conversion ratio would automatically be adjusted from to and the conversion price lowered from to . Also, if SVS sells common stock at a price below the conversion price, then the conversion price must be lowered (and the conversion ratio raised) to the price at which the new stock is issued. If protection were not contained in the contract, then a company could always prevent conversion by the use of stock splits and stock dividends. Warrants have similar protection against dilution.

However, this standard protection against dilution from selling new stock at prices below the conversion price can get a company into trouble. For example, SVS’s stock was selling for per share at the time the convertible was issued. Now suppose that the market went sour and the stock price dropped to per share. If SVS needs new equity to support operations, a new common stock sale would require the company to lower the conversion price on the convertible debentures from to . What impact would this have on the existing shareholders?

First, think about the value of a convertible bond as consisting of a straight bond and an option to convert. Reducing the conversion price is like reducing the strike price on an option, which would make the option to convert much more valuable. Second, recall the approach taken by the free cash flow valuation model to determine the value of equity—start with the value of operations, add the value of any nonoperating assets (like T-bills), and subtract the value of any debt, including convertible bonds. We can estimate the value of equity at the original conversion price and compare it to the value of equity at the new conversion price. At the new conversion price, the value of the convertible bond goes up, so the value of equity goes down, causing a transfer of wealth from the existing shareholders to the convertible bond-holders. Therefore, the protective reset feature on the conversion price makes it very costly for existing shareholders to raise additional equity in the times when new equity is needed.

20-3b

The Component Cost of Convertibles

Resource

See Ch20 Tool Kit.xls on the textbook’s Web site for details.

Resource

For a more detailed discussion of call strategies, see Web Extension 20A on the textbook’s Web site.

In the spring of 2013, Silicon Valley Software was evaluating the use of the convertible bond issue described earlier. The issue would consist of convertible bonds that would sell at a price of per bond; this would also be the bond’s par (and maturity) value. The bonds would pay an annual coupon interest rate, which is . Each bond would be convertible into shares of stock, so the conversion price would be . Its stock price was . If the bonds were not made convertible then they would have to provide a yield of , given their risk and the general level of interest rates. The convertible bonds would not be callable for , after which they could be called at a price of , with this price declining by thereafter. If, after , the conversion value exceeded the call price by at least , management would probably call the bonds.

SVS’s cost of equity is , with a dividend yield and expected capital gain of (Silicon Valley Software is a high risk company with low dividends and occasional stock repurchases, so its stock price has a high expected growth rate).

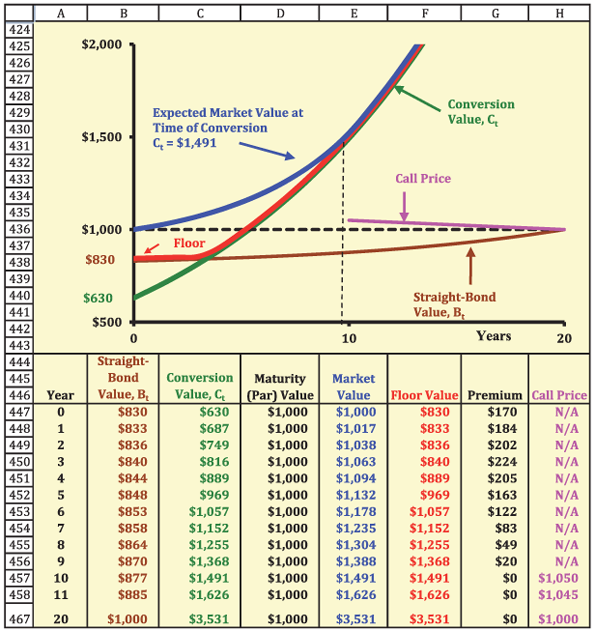

Figure 20-1 shows the expectations of both an average investor and the company. Refer to the figure as you consider the following points.

Figure 20-1

Silicon Valley Software: Convertible Bond Model

![]()

The horizontal dashed line at represents the par (and maturity) value. Also, is the price at which the bond is initially offered to the public.

The bond is protected against a call for . It is initially callable at a price of ; the call price declines thereafter by , as shown by the pink line in Figure 20-1.

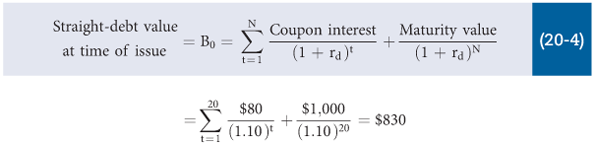

Because the convertible has an coupon rate and because the yield on a nonconvertible bond of similar risk is , it follows that the expected “straight-bond” value of the convertible, , must be less than par. At the time of issue and assuming an annual coupon, is :

![Discussion/ Chapter Summary Chapters 10,11 and 20 10]() (20-4)

Note, however, that the bond’s straight-debt value must be at maturity, so the straight-debt value rises over time; this is plotted by the brown line in Figure 20-1.

(20-4)

Note, however, that the bond’s straight-debt value must be at maturity, so the straight-debt value rises over time; this is plotted by the brown line in Figure 20-1.The bond’s initial conversion value, , or the value of the stock an investor would receive if the bonds were converted at , is . Because the stock price is expected to grow at a rate, the conversion value should rise over time. For example, in Year 5 it should be . The expected conversion value is shown by the green line in Figure 20-1.

If the market price dropped below the straight-bond value, then those who wanted bonds would recognize the bargain and buy the convertible as a bond. Similarly, if the market price dropped below the conversion value, people would buy the convertibles, exercise them to get stock, and then sell the stock at a profit. Therefore, the higher of the bond value and conversion value curves in the graph represents a floor price for the bond. In Figure 20-1, the floor price is represented by the red line.

The convertible bond’s market price will exceed the straight-bond value because the option to convert is worth something—an bond with conversion possibilities is worth more than an bond without this option. The convertible’s price will also exceed its conversion value because holding the convertible is equivalent to holding a call option and, prior to expiration, the option’s true value is higher than its exercise (or conversion) value. Without using financial engineering models, we cannot say exactly where the market value line will lie, but as a rule it will be above the floor, as shown by the blue line in Figure 20-1.

If the stock price continues to increase, then it becomes more and more likely that the bond will be converted. As this likelihood increases, the market value line will begin to converge with the conversion value line. After the bond becomes callable, its market value cannot exceed the higher of the conversion value and the call price without exposing investors to the danger of a call. For example, suppose that after issue (when the bonds become callable) the market value of the bond is , the conversion value is , and the call price is . If the company called the bonds the day after you bought one for , you would choose to convert them to stock worth only (rather than let the company buy the bond from you at the call price), so you would suffer a loss of . Recognizing this danger, you and other investors would refuse to pay a premium over the higher of the call price or the conversion value after the bond becomes callable. Therefore, in Figure 20-1, we assume that the market value line hits the conversion value line in Year 10, when the bond becomes callable.

In our example, the call-protection period ends in . At this time, the expected stock price is so high that the conversion value is almost certainly going to be greater than the call price; hence we assume that the bond will be converted immediately prior to the company calling the bond, which would happen in .

The expected market value at Year 10 is . An investor can find the expected rate of return on the convertible bond, , by finding the of the following cash flow stream:

![Discussion/ Chapter Summary Chapters 10,11 and 20 11]() With a financial calculator, we set , , , and ; we then solve for .

With a financial calculator, we set , , , and ; we then solve for .

(20-4)

Note, however, that the bond’s straight-debt value must be at maturity, so the straight-debt value rises over time; this is plotted by the brown line in Figure 20-1.

(20-4)

Note, however, that the bond’s straight-debt value must be at maturity, so the straight-debt value rises over time; this is plotted by the brown line in Figure 20-1. With a financial calculator, we set , , , and ; we then solve for .

With a financial calculator, we set , , , and ; we then solve for . A convertible bond is riskier than straight debt but less risky than stock, so its cost of capital should be somewhere between the cost of straight debt and the cost of equity. This is true in our example: , , and .![]()

20-3c

Use of Convertibles in Financing

Convertibles have two important advantages from the issuer’s standpoint:

(1) Convertibles, like bonds with warrants, offer a company the chance to sell debt with a low coupon rate in exchange for giving bondholders a chance to participate in the company’s success if it does well.

(2) In a sense, convertibles provide a way to sell common stock at prices higher than those currently prevailing.

Some companies actually want to sell common stock, not debt, but feel that the price of their stock is temporarily depressed. Management may know, for example, that earnings are depressed because of start-up costs associated with a new project, but they expect earnings to rise sharply during the next year or so, pulling the price of the stock up with them. Thus, if the company sold stock now, it would be giving up more shares than necessary to raise a given amount of capital. However, if it set the conversion price to above the present market price of the stock, then to fewer shares would be given up when the bonds were converted than if stock were sold directly at the current time. Note, however, that management is counting on the stock’s price to rise above the conversion price, thus making the bonds attractive in conversion. If earnings do not rise and pull the stock price up, so that conversion does not occur, then the company will be saddled with debt in the face of low earnings, which could be disastrous.

How can the company be sure that conversion will occur if the price of the stock rises above the conversion price? Typically, convertibles contain a call provision that enables the issuing firm to force holders to convert. Suppose the conversion price is , the conversion ratio is , the market price of the common stock has risen to , and the call price on a convertible bond is . If the company calls the bond, bondholders can either convert into common stock with a market value of or allow the company to redeem the bond for . Naturally, bondholders prefer to , so conversion would occur. The call provision thus gives the company a way to force conversion, provided the market price of the stock is greater than the conversion price. Note, however, that most convertibles have a fairly long period of call protection— is typical. Therefore, if the company wants to be able to force conversion early, it will have to set a short call-protection period. This will, in turn, require that it set a higher coupon rate or a lower conversion price.

From the standpoint of the issuer, convertibles have three important disadvantages:

(1) Even though the use of a convertible bond may give the company the opportunity to sell stock at a price higher than the current price, if the stock greatly increases in price, then the firm would be better off if it had used straight debt (in spite of its higher cost) and then later sold common stock and refunded the debt.

(2) Convertibles typically have a low coupon interest rate, and the advantage of this low-cost debt will be lost when conversion occurs.

(3) If the company truly wants to raise equity capital and if the price of the stock does not rise sufficiently after the bond is issued, then the company will be stuck with debt.

20-3d

Convertibles and Agency Costs

A potential agency conflict between bondholders and stockholders is asset substitution, also known as “bait and switch.” Suppose a company has been investing in low-risk projects, and because risk is low, bondholders charge a low interest rate. What happens if the company is considering a very risky but highly profitable venture that potential lenders don’t know about? The company might decide to raise low-interest-rate debt without revealing that the funds will be invested in a risky project. After the funds have been raised and the investment is made, the value of the debt should fall because its interest rate will be too low to compensate debtholders for the high risk they bear. This is a “heads I win, tails you lose” situation, and it results in a wealth transfer from bondholders to stockholders.

Let’s use some numbers to illustrate this scenario. The value of a company, based on the present value of its future free cash flows, is . It has of debt, based on market values. Therefore, its equity is worth . The company now undertakes some projects with high but risky expected returns, and its expected NPV remains unchanged. In other words, the actual NPV will probably end up much higher or much lower than under the old situation, but the firm still has the same expected value. Even though its total value is still , the value of the debt falls because its risk has increased. Note that the debtholders don’t benefit if the venture’s value is higher than expected, because the most they can receive is the contracted coupon and the principal repayment. However, they will suffer if the value of the projects turns out to be lower than expected, because they might not receive the full value of their contracted payments. In other words, risk doesn’t give them any upside potential but does expose them to downside losses, so the bondholders’ expected value must decline.

With a constant total firm value, if the value of the debt falls from to , then the value of equity must increase from to . Thus, the bait-and-switch tactic causes a wealth transfer of from debtholders to stockholders.

If debtholders think a company might employ the bait-and-switch tactic, they will charge a higher interest rate, and this higher interest rate is an agency cost. Debtholders will charge this higher rate even if the company has no intention of engaging in bait-and-switch behavior, because they can’t know the company’s true intentions. Therefore, they assume the worst and charge a higher interest rate.

Convertible securities are one way to mitigate this type of agency cost. Suppose the debt is convertible and the company does take on the high-risk project. If the value of the company turns out to be higher than expected, then bondholders can convert their debt to equity and benefit from the successful investment. Therefore, bondholders are willing to charge a lower interest rate on convertibles, and this serves to minimize the agency costs.

Note that if a company does not engage in bait-and-switch behavior by swapping low-risk projects for high-risk projects, then the chance of “hitting a home run” is reduced. Because there is less chance of a home run, the convertible bond is less likely to be converted. In this situation, the convertible bonds are actually similar to nonconvertible debt, except that they carry a lower interest rate.

Now consider a different agency cost, one due to asymmetric information between the managers and potential new stockholders. Suppose a firm’s managers know that its future prospects are not as good as the market believes, which means the current stock price is too high. Acting in the interests of existing stockholders, managers can issue stock at the current high price. When the poor future prospects are eventually revealed, the stock price will fall, causing a transfer of wealth from the new shareholders to old shareholders.

To illustrate this, suppose the market estimates an present value of future free cash flows. For simplicity, assume the firm has no nonoperating assets and no debt, so the total value of both the firm and the equity is . However, its managers know the market has overestimated the future free cash flows and that the true value is only . When investors eventually discover this, the value of the company will drop to . But before this happens, suppose the company raises of new equity. The company uses this new cash to invest in projects with a present value of , which shouldn’t be too hard, because these projects have a zero NPV. Right after the new stock is sold, the company will have a market value of , based on the market’s overly optimistic estimate of the company’s future prospects. Observe that the new shareholders own of the company and the original shareholders own .

As time passes, the market will realize that the previously estimated value of for the company’s original set of projects was too high and that these projects are worth only . The new projects are still worth , so the total value of the company will fall to . The original shareholders’ value is now of , which is . Note that this is more than it would have been if the company had issued no new stock. The new shareholders’ value is now , which is less than their original investment. The net effect is a wealth transfer from the new shareholders to the original shareholders.

Because potential shareholders know this might occur, they interpret an issue of new stock as a signal of poor future prospects, which causes the stock price to fall. Note also that this will occur even for companies whose future prospects are actually quite good, because the market has no way of distinguishing between companies with good versus poor prospects.

A company with good future prospects might want to issue equity, but it knows the market will interpret this as a negative signal. One way to obtain equity and yet avoid this signaling effect is to issue convertible bonds. Because the company knows its true future prospects are better than the market anticipates, it knows the bonds will likely end up being converted to equity. Thus, a company in this situation is issuing equity “through the back door” when it issues convertible debt.

In summary, convertibles are logical securities to use in at least two situations. First, if a company would like to finance with straight debt but lenders are afraid the funds will be invested in a manner that increases the firm’s risk profile, then convertibles are a good choice. Second, if a company wants to issue stock but thinks such a move would cause investors to interpret a stock offering as a signal of tough times ahead, then again convertibles would be a good choice.![]()

20-4

A Final Comparison of Warrants and Convertibles

Convertible debt can be thought of as straight debt with nondetachable warrants. Thus, at first blush, it might appear that debt with warrants and convertible debt are more or less interchangeable. However, a closer look reveals one major and several minor differences between these two securities.![]() First, as we discussed previously, the exercise of warrants brings in new equity capital, whereas the conversion of convertibles results only in an accounting transfer.

First, as we discussed previously, the exercise of warrants brings in new equity capital, whereas the conversion of convertibles results only in an accounting transfer.

A second difference involves flexibility. Most convertibles contain a call provision that allows the issuer either to refund the debt or to force conversion, depending on the relationship between the conversion value and call price. However, most warrants are not callable, so firms must wait until maturity for the warrants to generate new equity capital. Generally, maturities also differ between warrants and convertibles. Warrants typically have much shorter maturities than convertibles, and warrants typically expire before their accompanying debt matures. Warrants also provide for fewer future common shares than do convertibles, because with convertibles all of the debt is converted to stock, whereas debt remains outstanding when warrants are exercised. Together, these facts suggest that debt-plus-warrant issuers are actually more interested in selling debt than in selling equity.

In general, firms that issue debt with warrants are smaller and riskier than those that issue convertibles. One possible rationale for the use of option securities, especially the use of debt with warrants by small firms, is the difficulty investors have in assessing the risk of small companies. If a start-up with a new, untested product seeks debt financing, then it’s difficult for potential lenders to judge the riskiness of the venture and so it’s difficult to set a fair interest rate. Under these circumstances, many potential investors will be reluctant to invest, making it necessary to set a very high interest rate to attract debt capital. By issuing debt with warrants, investors obtain a package that offers upside potential to offset the risks of loss.

Finally, there is a significant difference in issuance costs between debt with warrants and convertible debt. Bonds with warrants typically require issuance costs that are about points more than the flotation costs for convertibles. In general, bond-with-warrant financings have underwriting fees that approximate the weighted average of the fees associated with debt and equity issues, whereas underwriting costs for convertibles are more like those associated with straight debt.

20-5

Reporting Earnings When Warrants or Convertibles Are Outstanding

If warrants or convertibles are outstanding, the Financial Accounting Standard Board requires that a firm report basic earnings per share and diluted earnings per share.![]()

Basic EPS is calculated as earnings available to common stockholders divided by the average number of shares actually outstanding during the period.

Diluted EPS is calculated as the earnings that would have been available to common shareholders divided by the average number of shares that would have been outstanding if “dilutive” securities had been converted. The rules governing the calculation of diluted EPS are quite complex; here we present a simple illustration using convertible bonds. If the bonds had been converted at the beginning of the accounting period, then the firm’s interest payments would have been lower because it would not have had to pay interest on the bonds, and this would have caused earnings to be higher. But the number of outstanding shares of stock also would have increased because of the conversion. If the higher earnings and higher number of shares caused EPS to fall, then the convertible bonds would be defined as dilutive securities because their conversion would decrease (or dilute) EPS. All convertible securities with a net dilutive effect are included when calculating diluted EPS. Therefore, this definition means that diluted EPS always will be lower than basic EPS. In essence, the diluted EPS measure is an attempt to show how the presence of convertible securities reduces common shareholders’ claims on the firm.

Under SEC rules, firms are required to report both basic and diluted EPS. For firms with large amounts of option securities outstanding, there can be a substantial difference between the basic and diluted EPS figures. This makes it easier for investors to compare the performance of U.S. firms with their foreign counterparts, which tend to use basic EPS.