Auditing assignments.

0Illustrative Audit Case: Keystone Computers Networks, Inc.

Part IV: Consideration of Internal Control

This part of the audit case of Keystone Computers ’ Networks, Inc. (KCN), illustrates the nature of internal control over the acquisition cycle and the way in which auditors assess control risk for this cycle. The following working papers are included:

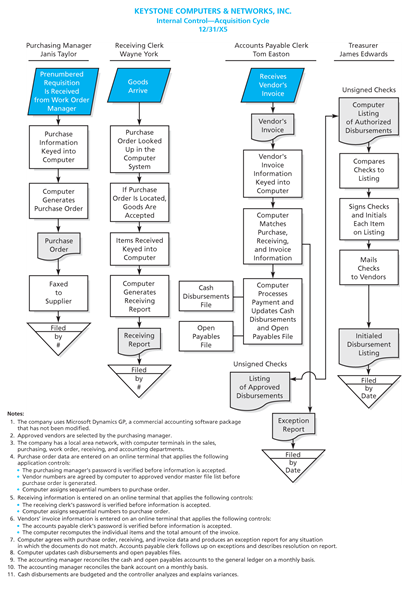

A flowchart description of the acquisition cycle of the company and the related controls prepared by the staff of Adams, Barnes ’ Co. (ABC), CPAs. This flowchart focuses on the (accounting) information system and control activities.

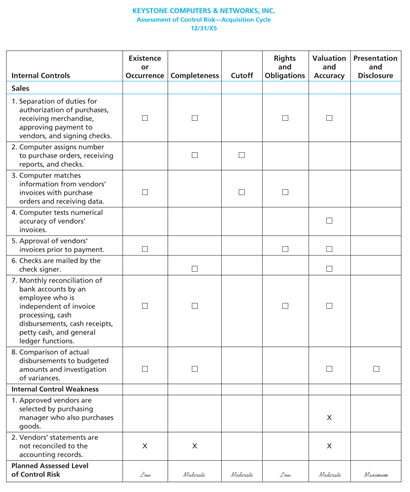

ABC’s working paper for the assessment of control risk for accounts payable and purchases as it would appear before any tests of controls are performed. This working paper identifies the prescribed controls and weaknesses for the revenue cycle. It also relates the controls and weaknesses to the various financial statement assertions about accounts payable and purchases.

You should read through the information to obtain an understanding of typical controls for this cycle. You may also wish to review the planning documentation presented on pages 240–247 of Chapter 6 to refresh your knowledge about the nature of the company’s business and its environment. The Control Environment, Risk Assessment, and Monitoring Questionnaire on pages 489–490 and the Organizational Chart of KCN on page 491 can be used to help refresh your memory about these components of internal control.

Appendix 14A Problems

A summary of the controls for the acquisition cycle of Keystone Computers Networks, Inc., appears above.

Required:

For the following three controls over the acquisition cycle, indicate one type of error or fraud that the control serves to prevent or detect. Organize your solution as follows:

| Control | Error or Fraud Controlled | ||

| 1. | Computer matches information from vendors’ invoice with purchase order and receiving data. |

| |

| 2. | The computer assigns numbers to receiving reports. |

| |

| 3. | Checks are mailed by check signer. |

| |

For each of the controls described above, indicate how the auditors could test the control. Organize your answer as follows:

Control

Tests of Controls

1.

Computer matches information from vendors’ invoice with purchase order and receiving data.

2.

The computer assigns numbers to receiving reports.

3.

Checks are mailed by check signer.

As indicated on the control risk assessment working paper, the auditors identified two weaknesses in internal control over the acquisition cycle of KCN. Describe the implications of each of the two weaknesses in terms of the type of errors or fraud that could result.

The auditors’ working paper that relates control strengths and weaknesses to the assertions about purchases and accounts payable is presented above. This working paper also presents the auditors’ planned assessed level of control risk for each of the assertions.

Prepare an audit plan for tests of the controls over the acquisition cycle. (Note: You may want to use the tests of controls plan for the revenue cycle, which is on pages 496–497, as a guide.)