Cases to Accompany the Financial Accounting Research System (FARS) Outline Case 1: New Financing: Do Credit Agreements Pose Unique Accounting and

Cases to Accompany the Financial Accounting Research System (FARS)

Outline

Case 1: New Financing: Do Credit Agreements Pose Unique Accounting and Disclosure Challenges? Gunther International

Case 2: Microsoft: Does Income Statement Classification Matter?

Case 3: Charitable Contributions and Debt: A Comparison of St. Jude Children's Research Hospital/ALSAC and Universal Health Services

Case 4: Clarus Corporation: Recurring Revenue Recognition

Case 5: When Would Market to Book Be Less Than One? Does Acquisition by Stock Explain JDS Uniphase Corp.?

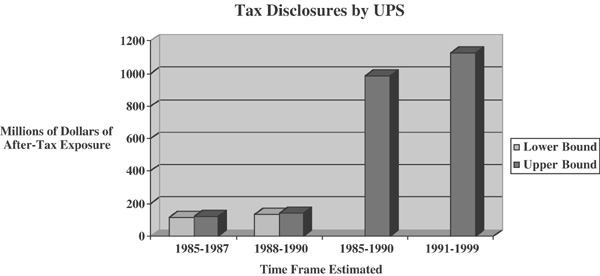

Case 6: UPS: The Tax Environment and Disclosure of Contingencies

Case 7: Embezzlement-Related Disclosures: Compliance with Guidance?

Case 8: What Constitutes a Subsequent Event? Related Gain Contingency Considerations

Case 9: Reconciling International Practices to Those of the FASB: Cash Flow

Case 10: Is the Asset Impaired—or Perhaps a Big Bath?

Case 11: Financial Instruments and Hedging: Measurement Challenges

Case 12: Emerging Issues: The Agenda of FASB

Figures and Tables

Figure 5.6-1 A number of estimates are disclosed in the 10-Q

Table 5.1-1 Summary Financial Data—Income Statement Related

Table 5.1-2 Summary Financial Data—Balance Sheet Related

Table 5.2-1 Reclassified Historical Income Statements by Year

Table 5.3-1 Financial Comparisons of the Not-for-Profit Entities

Table 5.3-2 Universal Health Services, Inc.'s Financial Excerpts

Table 5.3-3 Patient Revenue Mix

Table 5.4-1 Financial Information

Table 5.5-1 Acquisitions of JDS Uniphase Corp.

Table 5.7-1 Excerpts from Results of Operations

Table 5.7-2 Factors that May Affect Future Results

Table 5.8-1 Liabilities and Stockholders' Deficit Excerpts from Consolidated Balance Sheet (Unaudited)

Table 5.8-2 Excerpts from Euronet Worldwide, Inc. and Subsidiaries Consolidated Statements of Operations and Comprehensive Income/(Loss) (Unaudited)

Table 5.9-1 Financial Statement Terminology

Table 5.9-2 Consolidated Cash Flow Statement for the Six Months Ended 30 June 2001

Table 5.10-1 FleetBoston Financial Corp. Consolidated Statements of Income (Unaudited)

Table 5.10-2 Excerpt from FleetBoston Financial Corp. Consolidated Balance Sheets (Unaudited)

Case 1New Financing: Do Credit Agreements Pose Unique Accounting and Disclosure Challenges? Gunther International

Case Topics Outline

Terms of New Credit Arrangement

Restructuring

Guarantors

Collateral

Subordination

Warrants

Valuation

Disclosure

Context

Rights Offering

Gunther International has had a rocky road, financially. You joined the company upon graduation and recall having heard about it being significantly restructured in September 1992. It was then that two shareholders assumed control of the corporation and infused additional capital. Your department has been rocked by recent discoveries of accounting issues that have caused a delay in reported numbers. You assisted in crafting the language that appeared in the 8-K filing:

Item 5. Other Events.

On June 23, 1998, the registrant issued a press release announcing that it does not expect to release its final results for the fourth quarter and the full fiscal year ended March 31, 1998 until later in July 1998. A copy of the press release is attached hereto as an exhibit. During the course of the year-end audit, the Company's auditors, Arthur Andersen LLP, identified errors in the accumulation of contract costs and certain items of expense that were not properly accounted for. The Company, with the assistance of its auditors, is continuing to review the nature and extent of these matters, as well as the effect these matters may have on the Company's financial results. Based on the information that is available at this time, the Company currently expects to report a net loss for the fiscal year ended March 31, 1998 of approximately $2.4 to $3.0 million. The Company also expects to restate its results for each of the first three quarters of fiscal 1998. Previously issued financial statements for the interim periods of fiscal 1998 should not be relied upon.

The net losses referred to above are expected to result in a violation of certain financial covenants contained in the Company's senior credit facility. The Company has informed representatives of its senior lender about these matters and intends to meet with them to discuss a satisfactory resolution of the situation. If a satisfactory resolution is not reached, the Company may suffer an event of default under its senior credit facility and the Company's ability to continue to borrow thereunder may be impaired.

The Company is moving forward at an aggressive pace to definitively announce its financial results as quickly as possible. The Company continues to maintain a large installed base of customers using its products and believes that its products continue to be well received in the market place. The Company expects to have a record backlog of sales under contract in excess of $5 million as of June 30, 1998.

The Company's expectations are preliminary and are subject to the completion of its year-end audit. The estimated amount of loss, anticipated release of final results and the potential consequences of these matters, including without limitation the resolution of expected violations under the Company's senior credit facility discussed in this report constitute forward-looking statements, and the Company's actual results could differ from those discussed above ….(Source: 8-K filed 6/23/98)

As the 8-K suggests, a good deal of uncertainty surrounds the financing arrangements of the company going forward. The treasurer's department has been working long hours to explore the options. They requested financial numbers under the existing, though somewhat tenuous financing arrangement. While in preliminary form, assume you have access to something similar to what eventually appeared as the restated financial disclosures in Tables 5.1‐1 and 5.1‐2.

Table 5.1-1. Summary Financial Data—Income Statement Related *

|

| Year Ended March 31, 1998 | Year Ended March 31, 1997 | Year Ended March 31, 1996 |

| Sales: |

|

|

|

| Systems | $ 8,630,103 | $ 8,716,473 | $ 8,458,700 |

| Maintenance | 6,454,716 | 4,911,794 | 4,022,562 |

| Total Sales | 15,084,819 | 13,628,267 | 12,481,262 |

| Cost of Sales: |

|

|

|

| Systems | 7,030,092 | 5,573,323 | 5,821,526 |

| Maintenance | 4,771,692 | 4,088,858 | 2,826,853 |

| Total Cost of Sales | 11,801,784 | 9,662,181 | 8,648,379 |

| Gross Profit | 3,283,035 | 3,966,086 | 3,832,883 |

| Operating Expenses: |

|

|

|

| Selling and Administrative | 5,050,863 | 4,680,946 | 4,213,832 |

| Research and Development | 618,735 | 435,404 | 255,243 |

| Total Operating Expenses | 5,669,598 | 5,116,350 | 4,469,075 |

| Operating Loss | (2,386,563) | (1,150,264) | (636,192) |

| Other Expenses: |

|

|

|

| Interest Expense, Net | (245,552) | (184,426) | (243,363) |

| Net Loss | $(2,632,115) | $(1,334,690) | $(879,555) |

| Net Loss Per Share | $ (0.61) | $ (0.32) | $ (0.23) |

*The summary financial data presented should be read in conjunction with the information set forth in the financial statements and notes thereto.Source: January 14, 1999 10-KSB/A filing by Gunther International.

Table 5.1-2. Summary Financial Data—Balance Sheet Related *

|

| 1998 (As Restated) | 1997 (As Restated) |

| Current Assets | $3,118,386 | $3,616,493 |

| Total Assets | 8,036,929 | 8,663,040 |

| Current Liabilities | 7,981,871 | 5,661,800 |

| Long-Term Debt, less current maturities | 1,884,551 | 2,213,618 |

| Stockholders' Equity (Deficit) | (1,829,493) | 787,622 |

*The summary financial data presented should be read in conjunction with the information set forth in the financial statements and notes thereto.Source: January 14, 1999 10-KSB/A filing by Gunther International.

The reason for the tenuous situation with the creditors is the reported error that resulted in the debt covenant violations on the line of credit held by Bank of Boston. Credit agreements, often the lifeblood of a company, can take a variety of forms, with diverse covenants and commitments. Gunther's solution to this covenant violation has been to find new financing and pay off the line of credit with the Bank of Boston. You have worked with colleagues in both the controller's office and the treasurer's department to craft the following language for inclusion in yet another 8-K filing:

GUNTHER ANNOUNCES COMPLETION OF COMPREHENSIVE FINANCING TRANSACTION

NORWICH, CT (October 2, 1998)—Gunther International, Ltd. (NASDAQ: SORT) today announced it has successfully completed a comprehensive $5.7 million financing transaction, the proceeds of which have been utilized to completely restructure and replace the Company's pre-existing senior line of credit, fund a full settlement with the Company's third party service provider, and provide additional working capital to fund the Company's ongoing business operations.

Under the terms of the transaction, a newly formed limited liability company organized by the Tisch Family Interests and Mr. Robert Spiegel (the “New Lender”) loaned an aggregate of $4 million to the Company. At the same time, the Company's senior lender reached an agreement with the guarantor of a portion of the Company's senior line of credit (the “Guarantor”) whereby the Guarantor consented to the liquidation of approximately $1.7 million of collateral and the application of the proceeds of such collateral to satisfy and repay in full a like amount of indebtedness outstanding under the senior credit facility. The balance of the indebtedness outstanding under the senior credit facility, approximating $350,000, was repaid in full from the proceeds of the new financing. The Company executed a new promissory note in favor of the Guarantor evidencing the Company's obligation to repay the amount of the collateral that was liquidated by the senior lender. The Company's obligations to the Guarantor are completely subordinated to the Company's obligations to the New Lender. In addition, approximately $1.4 million of the new financing was utilized to pay the Company's third party service provider all amounts that were due and owing to the service provider for performing maintenance on Company systems.

To induce the New Lender to enter into the financing transaction, the Company, the New Lender, Park Investment Partners, Gerald H. Newman, the estate of Harold S. Geneen (the “Estate”), Four Partners, and Robert Spiegel Entered into a separate voting agreement, pursuant to which they each agreed to vote all shares of Gunther stock held by them in favor of (i) that number of persons nominated by the New Lender constituting a majority of the Board of Directors, (ii) one person nominated by the Estate and (iii) one person nominated by Park Investment Partners. In addition, the Company granted the New Lender a stock purchase warrant entitling the New Lender, any time during the period commencing on January 1, 1999 and ending on the fifth anniversary of the transaction, to purchase up to 35% of the pro forma, fully diluted number of shares of the Common Stock of the Company, determined as of the date of exercise. The exercise price of the warrant is $1.50 per share.

Contemporaneously with the consummation of the transaction, Frederick W. Kolling III and James H. Whitney resigned from the Board of Directors, and Thomas Steinberg and Robert Spiegel were elected to fill the vacancies created by the resignations. Another inside director, Alan W. Morton, resigned from the Board prior to the consummation of the transactions.

The Company is continuing to review the previously announced issues regarding the accumulation of contract costs and the recognition of revenues and expenses relating to the Company's systems business. The Company expects to be in a position to release information concerning the results of the review by the end of October.

Gunther International, Ltd. is a leading manufacturer of intelligent document finishing systems and ink jet printing solutions. (Source: 8-K, filed 10/7/98)

Requirement A.1: Disclosure

As soon as the 8-K is released, the company's attention is directed toward the anticipated filing of a 10-K, which will need to provide full disclosure concerning this new financing arrangement in accordance with generally accepted accounting principles (GAAP). You have been asked to outline all associated accounting and disclosure issues that arise as a result of this transaction. The intent is that your outline will become a basis for a joint presentation with the controller to the board of directors.

List all relevant FARS references in the order of relevance to the transaction.

Clearly set forth permissible alternatives.

Draft your recommendation, as to both accounting for and disclosing of the transaction.

Hints Regarding Solution

Develop a comprehensive list of search words associated with the transaction.

Consider how the former arrangement might have been recorded in comparison to the current transaction, including potential balance sheet, income statement, and cash flow implications.

Consider broader disclosure requirements' association with particular transactions.

Context matters to accounting and disclosure decisions. Carefully consider the inter-relationship of the two press releases, giving particular attention to the various stakeholders affected by your recommendations.

Requirement A.2: Interdisciplinary Considerations

The board of directors is expected to be very interested in details concerning the transaction, making it imperative that interdisciplinary considerations be discussed as a part of your presentation.

Why is corporate governance so interrelated with credit arrangements?

Why are warrants frequently integrated into lending contracts?

Do contracts in economic settings generally slip into default when problems with past representations in financial statements arise? Be specific.

What are the consequences of delaying financial statement information for four months or longer?

Describe and justify a management strategy for Gunther International, in light of these past events.

Requirement B: Subsequent Filings

On January 14, 1999, Gunther International filed a 10-KSB/A (accessible at http://www.sec.gov) that contained the following disclosures:

The undersigned registrant hereby amends its Annual Report on

Form 10-KSB for the fiscal year ended March 31, 1998 to amend Items 6 and 7 of Part II and Item 13 of Part III, as set forth in this amendment.

ITEM 6. MANAGEMENT'S DISCUSSION AND ANALYSIS OR PLAN OF OPERATIONS. SUMMARY OF RECENT EVENTS … The Audit Committee's review has since been completed and it has been determined that accounts receivable were overstated and accounts payable and deferred service revenues were understated at March 31, 1997 and costs and estimated earnings in excess of billings on uncompleted contracts were overstated at March 31, 1998. As a result, the accompanying financial statements and management's discussion and analysis of financial condition and results of operations include restated results as of and for the years ended March 31, 1997 and 1998. Also, certain amounts were reclassified between selling and administrative expenses, cost of sales, and research and development expenses to more appropriately reflect the results of operations. The effect of the restatement for the year ended March 31, 1997 was to reduce operating results to a net loss of $(1,334,690), or $(0.32) per share, from net income of $258,889, or $0.06 per share. The effect of the restatement for the year ended March 31, 1998 was to decrease the net loss to $(2,632,115), or $(0.61) per share, from a net loss of $(2,701,819), or $(0.63) per share.

On October 2, 1998, the Company entered into a $5.7 million comprehensive financing transaction with the Bank of Boston, Connecticut, N.A. (the “Bank”), the Estate of Harold S. Geneen (the “Estate”) and Gunther Partners LLC (the “New Lender”), the proceeds of which have been utilized to restructure and replace the Company's pre-existing senior line of credit, fund a full settlement with the Company's third party service provider and provide additional working capital to fund the Company's ongoing business operations. Under the terms of the transaction, the New Lender loaned an aggregate of $4.0 million to the Company. At the same time, the Bank reached an agreement with the Estate, which had guaranteed a portion of the Company's senior line of credit, whereby the Estate consented to the liquidation of approximately $1.7 million of collateral and the application of the proceeds of such collateral to satisfy and repay in full a like amount of indebtedness outstanding under the senior credit facility. The balance of the indebtedness outstanding under the senior credit facility, approximately $350,000, was repaid in full from the proceeds of the new financing. The Company executed a new promissory note in favor of the Estate evidencing the Company's obligation to repay the amount of the collateral that was liquidated by the Bank. The Company's obligations to the Estate are subordinated to the Company's obligations to the New Lender. The principal balance of the $4.0 million debt is to be repaid in monthly installments of $100,000 from November 1, 1998 and continuing to and including September 1, 1999, $400,000 on October 1, 1999 and the balance shall be due on October 1, 2003. Interest shall be paid quarterly, at the rate of 8% per annum, beginning January 1, 1999 and continuing until the principal and interest due is paid in full. The debt is secured by a first priority interest in all tangible and intangible property and a secondary interest in patents and trademarks….

The promissory note in favor of the Estate for approximately $1.7 million is to be repaid at the earlier of one year after the Company's obligations to the New Lender are paid in full or on October 2, 2004. Interest, at 5.44% per annum, shall accrue on principal and unpaid interest, which is added to the outstanding balance and is due at the time of principal payments. The indebtedness is secured by all tangible and intangible personal property of the Company but is subordinated to all rights of the New Lender. (Source: January 14, 1999, 10-KSB/A filing by Gunther International)

Given these subsequent disclosures, would you propose any adjustments to the accounting or disclosure suggestions you presented prior to the resolution of the restatement? Explain the basis for your response.

Would you expect the new lender to make any adjustments to the current contractual arrangement when the credit arrangement is reconsidered at renewal?

What would be the accounting or disclosure implications of your expectations? Explain how the following subsequent development might influence your expectations, if you were requested to update your evaluation as of July 1999.

On June 29, 1999, a 10-KSB filing states within the Management's Discussion and Analysis (Item 6, Subhead Liquidity and Capital Resources):

The company did not make its required payments on their respective due dates and certain other information required by the loan agreement was not provided to the New Lender. The New Lender waived these deficiencies. As of March 31, 1999, all amounts due on the debt had been paid….

In the event the Company is unable to meet its payment obligations through April 1, 2000, in accordance with the Note Loan and Security Agreement, the new Lender will be willing to renegotiate the payment terms based upon available cash flow such that the payment terms would be acceptable to both the Company and the Lender. (Source: 10-KSB filing 6/29/99)

Requirement C: The Aftermath

At fiscal year ended March 31, 2001, in its 10-KSB/A fiiling as of July 3, 2001, events associated with the past financing arrangements are detailed, alongside the following disclosure:

Through June 30, 1999, the Company had made principal payments to Gunther Partners LLC aggregating $800,000, plus interest. In September 1999, the Company experienced a deficiency in operating cash flow and Gunther Partners LLC agreed to lend the Company an additional $800,000 and to otherwise restructure the payment terms of the note. As amended, the outstanding balance due Gunther Partners LLC is due in principal installments of $200,000 commencing on October 1, 2001 through April 1, 2002; $100,000 on May 1, 2002; and $2,500,000 on October 1, 2003. If, at any time prior to October 1, 2001, the accumulated deficit of the Company improves by $1.0 million or more compared to the amount at June 30, 1999 of $14.4 million (a “Triggering Event”), then the principal payments otherwise due from October 1, 2001 through May 1, 2002 shall … become due in consecutive monthly installments beginning on the first day of the second month following the Triggering Event. On April 4, 2000, the Company borrowed an additional $500,000 from Gunther Partners LLC.

In June 2001, the Company entered into a recapitalization agreement (the “Recapitalization Agreement”) with the Estate, Gunther Partners LLC and certain other stockholders. The Recapitalization Agreement provides that the Company will effectuate a registered public offering (“Rights Offering”) of up to 16,000,000 shares of its Common Stock (the “Offered Shares”) to its existing stockholders by subscription right on a pro-rata basis at a subscription price of $0.50 per share. The rights to subscribe to the Offered Shares will be granted at a ratio to be determined by the Board of Directors of the Company (the “Basic Subscription Right”). In addition, the Company's stockholders will be granted the right to “oversubscribe” for additional shares not purchased by other stockholders, up to the total amount of the Offered Shares (the “Oversubscription Right”). In the event that the Company's stockholders, other than Gunther Partners LLC, do not subscribe for and purchase all 16,000,000 of the Offered Shares, Gunther Partners LLC will subscribe for and purchase from the Company in the Rights Offering a number of shares equal to 16,000,000 less the number of shares subscribed for stockholders other than Gunther Partners LLC, up to a maximum of 14,000,000 shares. The net proceeds of the Rights Offering (a minimum of $7 million less offering expenses), will be used to repay in full the notes payable to Gunther Partners LLC ($4.5 million) and a stockholder and director ($500,000), to purchase all notes payable to the Estate for a total of $500,000 and to purchase 919,568 shares of the Company's Common Stock held by the Estate for $137,935 (or $0.15 per share). The balance of the net proceeds from the Rights Offering will be used for general working capital purposes. (Source: Gunther International Ltd 10-KSB/A 7/30/2001)

How much of the net proceeds from the rights offering will likely be available for general working capital purposes?

Compare the terms of the rights offering to the warrants embedded in the earlier financing arrangement. Why do you believe a rights offering approach is being pursued rather than a shelf registration targeting new shareholders?

What disclosures would you recommend be made by the company related to its financing, liquidity, and capital resources?

Directed Self-Study

What happened to Gunther International on December 4, 2003? [Access http://sec.gov for the answer.]

balloon payment

a large final payment on a loan that is repaid in installments.

collateral

assets that agreement gives the creditor the right to repossess and/or to convert into cash if the borrower defaults on the lending arrangement; also referred to as security for a loan, leading to the terminology of secured debt

compound interest

distinguished from simple interest by reinvesting each interest payment in order to earn more interest

continuous compounding

assumes continuous compounding of interest rather than compounding at fixed intervals

cum rights

with rights or rights on, distinguished from ex rights

deficit

arises in retained earnings when the cumulation of all prior years' net income or losses, less dividends declared, is negative

ex rights

purchase of shares not entitled to the rights to buy shares in the company's rights issue

exercise price

the price at which the holder of a warrant or similar instrument is permitted to buy the stock or other instrument to which it is convertible or is transferable

funded debt

matures after more than one year

guarantor

that individual or entity promising to pay should the borrower default

line of credit

a credit arrangement that permits a borrower to obtain funds up to a certain amount with prespecified terms, and an associated cost for the unused line of credit

maturity

that date at which an agreement comes to an end, such as a bond, reaching that date on which repayment is demanded in the absence of a renewal

promissory note

a written agreement specifying the terms of the debt

restatement

adjustment of past reported financial statements

restructuring

when applied to debt, refers to the renegotiation of terms that could include extension of the due date of principal and interest payments, reduction in the rate of interest on existing debt, and/or forgiveness by creditors of a portion of principal or accrued interest; also applied to changes in strategy and operations of a company (e.g., downsizing)

rights offering

the issue of securities to current stockholders that is sometimes referred to as a privileged subscription issue

secured debt

refers to obligations that if defaulted upon, lead to a first claim on specified assets

subordination

refers to the rights of a party being legally set behind another's, such as subordination of debt meaning that claims would not be fulfilled until unsubordinated debt commitments were met; subordinated debt is often called junior debt, receiving payment only after senior debt has been paid in full

warrant

instrument permitting the purchase of a specified number of shares at a specified dollar amount

working capital

current assets less current liabilities (i.e., net working capital)

Further Readings

Adut, Davit, William H. Cready, Thomas J. Lopez. 2003. “Restructuring charges and CEO cash compensation: A reexamination.”The Accounting Review (78, 1, January), pp. 169–192.

Beatty, Anne, K. Ramesh, and Joseph Weber. 2002. “The importance of accounting changes in debt contracts: The cost of flexibility in covenant calculations.” Journal of Accounting and Economics (33, 2, June), pp. 205–227.

Beatty, Anne, and Joseph Weber. 2003. “The effects of debt contracting on voluntary accounting method changes.” The Accounting Review (78, 1, January), pp. 119–142.

Beneish, Messod D., and Eric Press. 1993. “Costs of technical violation of accounting-based covenants.” The Accounting Review(68, 2, April), pp. 233–257.

Benston, G.J., and L.D. Wall. 2005. “How should banks account for loan losses?” Journal of Accounting and Public Policy (24, 2, March/April), pp. 81–100.

Berger, A., and G. Udell. 1995. “Relationship lending and lines of credit in small firm finance.” Journal of Business (68, July), pp. 351–381.

Berle, A., and G. Means. 1932. The Modern Corporation and Private Property. New York: McMillian.

Bitler, M., A. Robb, and J. Wolken. 2001. “Financial services used by small businesses: Evidence from the 1998 survey of small business finances.” Federal Reserve Bulletin (April), pp. 183–205.

Black, B. 1992. “Institutional investors and corporate governance: The case for institutional voice.” Journal of Applied Corporate Finance (5), pp. 19–32.

Cravens, Karen S., and Wanda A. Wallace. 2001. “A framework for determining the influence of the corporate board of directors in accounting studies.” Corporate Governance: An International Review (9, 1, January), pp. 2–24 (Oxford: Blackwell Publishers).

Cravens, K. S., and W. A. Wallace. 1999. “Blue ribbon plan requires more disclosure to work.” Accounting Today (July 26–August 8), pp. 14, 17, 40, 41.

Diamond, D. 1991. “Monitoring the reputation: The choice between bank loans and directly placed debt.” Journal of Political Economy (99, 4), pp. 689–721.

Duru, A., S. A. Manis and D. M. Reeb. 2005. “Earnings-based bonus plans and the agency costs of debt.” Journal of Accounting and Public Policy (24, 5, September/October), pp. 431–447.

Guenther, D., and M. Willenborg. 1999. “Capital gains tax rates and the cost of capital for small business: Evidence from the IPO market.” Journal of Financial Economics (53), pp. 385–408.

Gul, Ferdinand A. and Sidney Leung. 2004. “Board leadership, outside directors' expertise and voluntary corporate disclosures.”Journal of Accounting and Public Policy (23, 5, September/October), pp. 351–379.

Jones, Denise A., and Wanda A. Wallace. 2005. “Existing disclosure challenges of IPO allocations: A research report.” Research in Accounting Regulation (18), pp. 107–126.

Lee, Edward, Konstantinos Stathopoulos, and Mark Hon. 2006. “Investigating the return predictability of changes in corporate borrowing.” Accounting and Business Research (36, 2), pp. 93–107.

Leftwich, R. 1983. “Accounting information in private markets: Evidence from private lending agreements.” Accounting Review (January) , pp. 23–42.

Moehrle, Stephen R. 2002. “Do firms use restructuring charge reversals to meet earnings targets?” The Accounting Review (77, 2, April), pp. 397–413.

Muzatko, Steven R., Karla M. Johnstone, Brian W. Mayhew, and Larry E. Rittenberg. 2004. “An empirical investigation of IPO underpricing and the change to the LLP organization of audit firms.” Auditing: A Journal of Practice and Theory (23, 1, March), pp. 53–67.

Opler, Tim C. 1993. “Controlling financial distress costs in leveraged buyouts with financial innovations.” Financial Management(Financial Distress Special Issue, September), pp. 79–93.

Petersen, M., and R. Rajan. 1994. “The benefits of lending relationships: Evidence from small business data.” Journal of Finance(49, March), pp. 3–37.

Press, E., and J. Weintrop. 1991. “Financial statement disclosure of accounting-based debt covenants.” Accounting Horizons(March), p. 70.

Reilly, David. 2006. “No more ‘stealth restating’—SEC forces companies to highlight earnings changes, not just tack them on to their newest filings.” Wall Street Journal (September 21), pp. C1, C3.

Shleifer, A., and R. W. Vishny. 1997. “A survey of corporate governance.” Journal of Finance (52, 2), pp. 737–783.

The Sarbanes-Oxley Act of 2002 . Pub. L. No. 107–204 (July 30) 116 Stat. 745. H.R. 3763. 15 USC 7201 note.

Scott, Jr., J. H. 1979. “Bankruptcy, secured debt, and optimal capital structure: reply.” Journal of Finance (March), pp. 254–260.

SEC. Final Rule: Improper Influence on Conduct of Audits Securities and Exchange Commission 17 CFR Part 240. 2003. [Release Nos. 34–47890, IC-26050; FR-71; File No. S7-39-02] RIN 3235-AI67 (June 26).

Sheikh, Aamer, and Wanda A. Wallace. 2005. “Certification in the presence of uncertainty.” Accounting Today (19, 2, January 24–February 6), pp. 36, 37.

Sheikh, Aamer, and Wanda A. Wallace. 2005. “The Sarbanes-Oxley certification requirement: Analyzing the comments.” The CPA Journal, Special Auditing Issue, “Innovations in Auditing”—Constructing the Future (November), pp. 36–42.

Smith, Jr., C. W., and J. B. Warner. 1979. “Bankruptcy, secured debt, and optimal capital structure: Comment.” Journal of Finance(March), pp. 247–251.

Smith, Jr., C. W., and J. B. Warner. 1979. “On financial contracting: An analysis of bond covenants.” Journal of Financial Economics (June), pp. 117–161.

Wallace, Wanda A. 2005. “Auditor changes and restatements: An analysis of recent history.” CPA Journal (LXXV, 3, March), pp. 30–33.

Wallace, Wanda A. 2004. “Auditor rotation: A bad governance idea,” Guest Column. Directors & Boards (28, 3, Spring), p. 14 [Also included in E-Briefing (1, 2, June 2004 online newsletter)]

Wallace, Wanda A. 2004. Risk Assessment by Internal Auditors Using Past Research on Bankruptcy: Applying Bankruptcy Models.Altamonte Springs, FL: The Institute of Internal Auditors Research Foundation.) [.PDF file and linked EXCEL worksheets available at: http://www.theiia.org/iia/index.cfm?doc_id=4619 .]

Wilkinson, B. R, and C. E. Clements. 2006. “Corporate governance mechanisms and the early-filing of CEO certification.” Journal of Accounting and Public Policy (25, 2, March/April), pp. 121–139.

Williamson, O. E. 1985. The Economic Institution of Capitalism: Firms, Markets and Relational Contracting. New York: Free Press.

Williamson, O. E. 1984. “Corporate governance.” Yale Law Journal (93), pp. 1197–1230.

Williamson, O. E. 1979. “Transaction-cost economics. The governance of contractual relations.” Journal of Law and Economics(22, 2), pp. 233–261.

Wyatt, Anne. 2005. “Accounting recognition of intangible assets: Theory and evidence on economic determinants.” Accounting Review (80, 3, July), pp. 967–1003.

“The creditors are a superstitious sect, great observers of set days and times. Blessed is he that expects nothing for he shall never be disappointed.

—Benjamin Franklin, Poor Richard's Almanac

Case 2Microsoft: Does Income Statement Classification Matter?

Case Topics Outline

Microsoft Disclosure

Primary Business Alignment

Direct Cost Recording

Consistency of Presentation

Microsoft filed its 10-K on September 28, 1999, and disclosed the following:

Reclassifications. The Company changed the way it reports revenue and costs associated with product support, consulting, MSN Internet access, and certification and training of system integrators. Amounts received from customers for these activities have been classified as revenue in a manner more consistent with Microsoft's primary businesses. Direct costs of these activities are classified as cost of revenue. Prior financial statements have been reclassified for consistent presentation. Certain other reclassifications have also been made for consistent presentation. (Source: 10-K filed 9/28/99)

The financial statements for 1999 and 1998, as originally reported and as reclassified, are reported in Table 5.2-1.

Table 5.2-1. Reclassified Historical Income Statements by Year *

| Microsoft Corporation Reclassified Income Statements (in millions; unaudited) | Reported 1999 | Reclassified 1999 | Reported 1998 | Reclassified 1998 |

| Revenue Operating expenses: | $13,222 | $13,983 | $14,484 | $15,262 |

| Cost of revenue | 1,090 | 2,145 | 1,197 | 2,460 |

| Research and development | 1,889 | 2,030 | 2,502 | 2,601 |

| Acquired in-process technology | 296 | 296 | ||

| Sales and marketing | 2,766 | 2,331 | 3,412 | 2,828 |

| General and administrative | 392 | 392 | 433 | 433 |

| Other expenses | 60 | 60 | 230 | 230 |

| Total operating expenses | 6,197 | 6,958 | 8,070 | 8,848 |

| Operating income | 7,025 | 7,025 | 6,414 | 6,414 |

| Investment income | 1,318 | 1,318 | 703 | 703 |

| Gain on sale | 160 | 160 | ||

| Income before income taxes | 8,503 | 8,503 | 7,117 | 7,117 |

| Provision for income taxes | 2,920 | 2,920 | 2,627 | 2,627 |

| Net income | $5,583 | $5,583 | $4,490 | $4,490 |

| Earnings per share: |

|

|

|

|

| Basic | $ 1.11 | $ 1.11 | $ 0.92 | $ 0.92 |

| Diluted | $ 1.02 | $ 1.02 | $ 0.84 | $ 0.84 |

*1997 Fiscal Year Reclassifications are likewise presented as reported and reclassified in the Microsoft filing.

Requirement: Disclosure and Strategy-Related Considerations

You are a personal financial advisor to a number of clients, one of whom is a sophisticated investor in Microsoft. The client, who just received the September 1999 10-K filing is perplexed as to the meaning of the reclassifications, reflected in Table 5.2-1. Moreover, given the earnings per share effects are zero, the client does not understand why the disclosure was made at all.

Explain why Microsoft has provided the detail evidenced in Table 5.2-1. Support your explanation with appropriate citations from FARS.

Do you believe that the type of disclosure provided by Microsoft was essential in order for the corporation to comply with GAAP? Why or why not?

Should business strategy influence the classification of revenue and associated costs in an information system? Give an example of how classification of revenue and associated costs might differ between two companies that provide services associated with system design, software development, Internet sites, and other products analogous to those of Microsoft.

Directed Self-Study

Access the June 30, 2006 annual report for Microsoft at sec.gov and determine if it contains any indication of reclassifications on the income statement. Compare and contrast the nature of any disclosures found to those profiled in the case.

Do Dell's Woes Relate to Classification?

On February 2, 2007, the Wall Street Journal reported “Dell's Woes Mount as Investors File Improper Accounting Suit” (by Don Clark, Christopher Lawton and John R. Wilke, p. A4). Do the allegations involve classification issues? Explain. Use FARS to evaluate each of the allegations.

consistency

comparability across time of generally accepted accounting principles' application

direct costs

those costs that fluctuate directly with the product, such as raw materials and direct labor used to create physical products

reclassifications

changes in the account used to record or present a transaction, event, or estimate

Further Readings

Alexander, David. 1999. “A benchmark for the adequacy of published financial statements.” Accounting and Business Research(29, 3), pp. 239–253.

Bell, Timothy, Frank Marrs, Ira Solomon, and Howard Thomas. 1997. Auditing Organizations Through a Strategic-Systems Lens.KPMG Peat Marwick LLP.

Cato, Sid. 1988. “Manager's Journal: When preparing annual reports, less is definitely not more.” Wall Street Journal (August 22), 1988 WL-WSJ 454421.

Doyle, Robert K., and F. Gordon Spoor. 1999. “How to start an investment advisory practice.” Journal of Accountancy (187, 1, January).

Golub, Steven J., and Robert J. Kueppers. 1983. Summary Reporting of Financial Information: Moving Toward More Readable Annual Reports (A Research Study Prepared for Financial Executives Research Foundation).

Jacobs, Sanford L. 1988. “Annual reports in short form fail to catch on.” Wall Street Journal (April 14), 1988-WL-WSJ 468976.

Littleton, A. C. 1953. Structure of Accounting Theory. American Accounting Association Monograph No. 5. Sarasota, FL: American Accounting Association, pp. 39–40, 44.

Price, Reneé, and Wanda A. Wallace. 2001. Shades of Materiality (The Canadian Certified General Accountants' Research Foundation, Research Monograph 24 published on CD-ROM).

Price, Reneé, and Wanda A. Wallace. 1996–1997. “Too many shades of materiality only serve to confuse.” Audit & Accounting Forum. Accounting Today (December 16– January 5), p. 61.

SEC. 2003. “Frequently asked questions regarding the use of non-GAAP financial measures.” Prepared by staff members in the Division of Corporation Finance. Washington, DC: U.S. SEC, (June 13).

SEC. 2003. SAB No. 103, Codification of Staff Accounting Bulletins (as posted May) — Topic 1: Financial Statements; Topic 2: Business Combinations; Topic 3: Senior Securities; Topic 4: Equity Accounts; Topic 5: Miscellaneous Accounting; Topic 6: Interpretations of Accounting Series Releases and Financial Reporting Releases; Topic 7: Real Estate Companies; Topic 8: Retail Companies; Topic 9: Finance Companies; Topic 10: Utility Companies; Topic 11: Miscellaneous Disclosure; Topic 12: Oil and Gas Producing Activities; Topic 13: Revenue Recognition.

SEC. 1995. WL 385858 (SEC Release No.) 59 SEC Docket 1556, Release No. 33–7183, Release No. 34-35893, Release No. IC-21, 166. “Use of abbreviated financial statements in documents delivered to investors pursuant to the Securities Act of 1933 and Securities Exchange Act of 1934.” File No. S7-13-95, RIN 3235-AG49, (June 27).

Visvanathan, Gnanakumar. 2006. “An empirical investigation of ‘closeness to cash’ as a determinant of earnings response coefficients.” Accounting and Business Research (36, 2), pp. 109–120.

Wallace, Wanda A. 2003. “Analyzing non-GAAP line items in income statements.” CPA Journal (LXXIII, 6, June), pp. 38–47.

Make the scheme of accounts conform with the operating organization of the enterprise, because accounting data can thus be made to reveal the results of management's use of its opportunities.

—A.C. Littleton

[Source: Structure of Accounting Theory, American Accounting Association Monograph No. 5 (Sarasota, FL: American Accounting Association, 1966), p. 191]

Case 3Charitable Contributions and Debt: A Comparison of St. Jude Children's Research Hospital/ALSAC and Universal Health Services

Case Topics Outline

St. Jude Children's Research Hospital/ALSAC

Primary Objective

Sources of Capital

Reporting Practices

Universal Health Services

Investor-Owned Hospital

Debt Including Leases

Comparison

Hospitals are an industry in which both not-for-profits and investor-owned facilities operate. The sources of capital available to the not-for-profits include charitable contributions and debt offerings—unless they are governmental, in which case, higher taxes are also an alternative. Debt availability is always, in part, a function of performance, and just as failures have arisen in both sectors, about one-third of the investor-owned hospitals have been described as losing money. Of interest is how can one effectively evaluate such an industry, with this type of diversity in organizational forms and capital availability? A necessary prerequisite to such an evaluation is to have a firm understanding of how charitable contributions are presented.

St. Jude Children's Research Hospital/ALSAC has the mission of finding cures for children with catastrophic diseases through research and treatment. For the fiscal year 1999, this entity reported total assets of $221,664,232 and income of $177,071,890. A Web site at http://www.stjude.org, as well as Guidestar's listing, references a Form 990 (Return of Organization Exempt from Income Tax) filing, availability of audited financial statements upon request, and information that the hospital has 2,100 employees and 350 volunteers. Founded in 1962, the organization seeks funds from contributions and grants for unrestricted operating expenses, specific projects, buildings, and endowments. More than 4,000 patients are seen annually, with a hospital maintaining 56 beds. The Form 990, Part III states that the hospital provided 15,231 inpatient days of care during the fiscal year and patients made 40,982 clinic visits. ALSAC is the American Lebanese Syrian Associated Charities, Inc., the fund-raising arm of St. Jude Children's Research Hospital. It reported 1999 total assets of $1,007,699,320 and income of $274,123,399. This organization reports the number of employees as 565 and the number of volunteers as 800,000. With its sole focus on the hospital, ALSAC's self-description explains that no child has ever been turned away due to an inability to pay for treatment and explains key accomplishments in the research area achieved by St. Jude's research and treatment of children with catastrophic diseases. What is borne out by the example of St. Jude is the fact that a review of the Form 990 filed for the fiscal year ending 6/30/99 indicates in Part VI the names of related organizations: ALSAC and St. Jude Hospital Foundation, both of which are tax exempt. To gain a sense of capital availability to a not-for-profit entity, affiliated entities must be considered. In addition, the role of volunteers is a source of human capital not effectively captured within the framework of financial statements for not-for-profits, as reflected in the Form 990 for the fiscal year ending 6/30/99 for ALSAC, which states in Part VI:

Unpaid volunteers have made significant contributions of their time, principally in fund-raising activities. The value of these services is not recognized in the financial statements since it is not susceptible to an objective measurement or valuation and because the activities of these volunteers are not subject to the operating supervision and control present in an employer/employee relationship.

Hence, as one evaluates capital sources and uses by not-for-profits, care is needed to consider affiliated organizations' role, total contributions, and the effect of volunteerism on the comparability between not-for-profit and investor-owned operations.

Universal Health Services, Inc. filed its 10-K on March 28, 2001, for the calendar year 2000, which includes comparative information for 1999. Analysts have described the company as the most aggressive company in the industry over the 1999–2001 time frame in making acquisitions, particularly of not-for-profit operations and investor-owned operations experiencing losses. The company is praised for it high operating leverage, the relatively small number of shareholders relative to the magnitude of total revenue, and stock price as a multiple of earnings. The company operates 59 hospitals and, as of 1999, had an average number of licensed beds of 4,806 at acute care hospitals and 1,976 at behavioral health centers, with patient days of 963,842 and 444,632, respectively. Of interest is a commentary on the competition found in the company's filing:

Competition

In all geographical areas in which the Company operates, there are other hospitals which provide services comparable to those offered by the Company's hospitals, some of which are owned by governmental agencies and supported by tax revenues, and others of which are owned by nonprofit corporations and may be supported to a large extent by endowments and charitable contributions. Such support is not available to the Company's hospitals. Certain of the Company's competitors have greater financial resources, are better equipped and offer a broader range of services than the Company. Outpatient treatment and diagnostic facilities, outpatient surgical centers and freestanding ambulatory surgical centers also impact the healthcare marketplace. In recent years, competition among healthcare providers for patients has intensified as hospital occupancy rates in the United States have declined due to, among other things, regulatory and technological changes, increasing use of managed care payment systems, cost containment pressures, a shift toward outpatient treatment and an increasing supply of physicians. The Company's strategies are designed, and management believes that its facilities are positioned, to be competitive under these changing circumstances. (Source: 10-K filed 3/28/2001)

Financial information is provided in Tables 5.3‐1 and 5.3‐2 for both the not-for-profit and the investor-owned hospitals.

Table 5.3-1. Financial Comparisons of the Not-for-Profit Entities

| Fiscal Year Ended 1999 | St. Jude Children's Research Hospital Form 990 * | American Lebanese Syrian Associated Charities, Inc. (ALSAC) Form 990 * |

| Contributions, gifts, grants and similar amounts received: Direct public support | $91,978,426 | $231,793,748 |

| Indirect public support |

| 2,906,934 |

| Government contributions (grants) | 31,469,447 |

|

| Program service revenue, including government fees and contracts (i.e., health insurance revenue) | 46,034,710 |

|

| Accounts receivable | 24,217,029 | 4,230,764 |

| Pledges receivable |

| 23,604,748 |

| Allowance for doubtful accounts | 9,363,328 |

|

| Program service expenses |

| 99,282,906 |

| Program service expenses: Research | 87,225,830 |

|

| Program service expenses: Education and training | 5,471,186 |

|

| Program service expenses: Medical Services | 93,735,602 |

|

| Reconciliation of revenue, gains, and other support to audited numbers: net unrealized gains on investments | −4,023,815 | 65,891,269 |

| Deferred grant revenue | 1,857,628 |

|

|

| (Statement 5) |

|

| Support from American Lebanese Syrian Associated Charities, Inc. | 91,978,426 | 91,978,426 |

|

| (Statement 7) | (paid per Statements 4, 6) |

| Excluded contributions |

| 2,746,295 |

|

|

| (Statement 1) |

| Excess or (deficit) for the year | −10,933,191 | 120,521,982 |

| Net assets or fund balances at end of year | 199,707,440 | 994,501,910 |

| Temporarily restricted |

| 15,715,890 |

| Permanently restricted | 14,000,000 | 247,147,826 |

| Total liabilities | 21,956,792 | 7,017,192 |

| Schedule of deferred debits & credits by contract (FAS 116 adjustment noted to result in this deferred revenue) | 157,628 |

|

*The GuideStar.org Web site (http://www.guidestar.org) provides access to Forms 990 in.PDF format.

Table 5.3-2. Universal Health Services, Inc.'s Financial Excerpts *

| Income Statements (in thousands) | Reported 1999 Calendar Year |

| Net revenues | $2,042,380 |

| Operating charges | 1,913,346 |

| Components: |

|

| Salaries, wages, and benefits | 793,529 |

| Provision for doubtful accounts | 166,139 |

| Lease and rental expense | 49,029 |

| Interest expense, net | 26,872 |

| Net income | 77,775 |

| Total assets | 1,497,973 |

| Total liabilities | 856,362 |

| Total retained earnings | 482,960 |

| Capital stock | 306 |

| Paid-in capital in excess of par | 158,345 |

*The 10-K filing as of 3/28/2001 at EDGAR (http://www.sec.gov/edgar.shtml) provides financial statement information for 2000 and 1999.

Requirement A: Recording Revenue

What is meant by the reference in Table 5.3-1 to an FAS 116 adjustment?

How are contributions recorded? Is there a distinction between pledges receivable and accounts receivable?

Are there circumstances when financial statements can quantify volunteers' services?

Can financial statement users of not-for-profit hospitals' financial statements expect to be fully informed regarding affiliated parties, such as the linkages between St. Jude Children's Research Hospital, ALSAC, and the foundation cited? Explain.

Requirement B: Revenue Mix (Strategy-Related Considerations)

The 10-K filing of Universal Health Services, Inc. describes the mix of revenue sources, as depicted in Table 5.3-3.

How does this revenue mix compare with the revenue blend of the not-for-profit entity, St. Jude Children's Research Hospital (ALSAC)? Access the latest SEC filing and compare the reported revenue mix; has it changed?

What does that imply as to the strategies of investor-owned hospitals in managing risk and ensuring adequate capital relative to not-for-profit entities? An opportunity exists to explore the greater social and political questions that are frequently debated about the compatibility of profit-oriented entities and quality of health care, relative to not-for-profit entities. As background, identify what the latest SEC filings report concerning charity care.

Table 5.3-3. Patient Revenue Mix

|

| PERCENTAGE OF NET PATIENT REVENUES | ||||

|

| 2000 | 1999 | 1998 | 1997 | 1996 |

| Third Party Payors |

|

|

|

|

|

| Medicare…………………………………. | 32.3% | 33.5% | 34.3% | 35.6% | 35.6% |

| Medicaid…………………………………. | 11.5% | 12.6% | 11.3% | 14.5% | 15.3% |

| Managed Care (HMOs and PPOs)… | 34.5% | 31.5% | 27.2% | 19.1% | N/A |

| Other Sources…………………………… | 21.7% | 22.4% | 27.2% | 30.8% | 49.1% |

| Total………………………………………. | 100% | 100% | 100% | 100% | 100% |

N/A-Not available (Source: 10-K filed 3/28/2001)

Directed Self-Study

Access the 10-Q (from http://sec.gov) for the quarterly period ended June 30, 2006 and explain how Hurricane Katrina affected Universal Health Services. The same 10-Q reports on a funding commitment the company has made to the alma mater of the Chairman of the Board of Directors and Chief Executive Officer. Describe the disclosure and explain why the event is an “Other Related Party Transaction.” [Download the 10-Q in text format and apply the Find capability in your word processor. Also access FARS and identify the guidance relevant to each event.]

Health Insurance, Public Policy, and Backdating

A key factor in the health care industry is health insurance. Public policy has debated universal health care, changes to governmental programs such as Medicare, adjustment of tax policy regarding employers' and employees' deduction for premiums, and alternative approaches to this sector of the economy. State and local governments, under a new accounting rule, have recently estimated their total retiree health bill to be about $1.1 trillion. Over the past decade, some governmental units used pension funds to help pay for double-digit growth in health care for retired public workers. Explain how accounting interacts with public policy. Use FARS as a resource, according particular attention to FAS 158.

Health insurer UnitedHealth has been the focus of media coverage involving what is known as the “options backdating scandal”. UnitedHealth's internal probe estimates its past decade exposure at half a billion dollars (“UnitedHealth Faces Formal Probe,” Wall Street Journal, December 27, 2006, p. B8). Is there a relationship between the magnitude of the restatement and the nature of the health care sector of the economy? Explain. The SEC's Division of Corporation Finance shared a “Sample Letter Sent in Response to Inquiries Related to Filing Restated Financial Statements for Errors in Accounting for Stock Option Grants” dated January 2007 (http://www.sec.gov/divisions/corpfin/guidance/oilgasltr012007.htm.) How helpful do you find such guidance?

fund balance

“refers … to a common group of assets and related liabilities within a not-for-profit organization and to the net amount of those assets and liabilities…. While some not-for-profit organizations may choose to classify assets and liabilities into fund groups, information about those groupings is not a necessary part of general purpose external financial reporting” (CON6, Footnote 45); fund balances may refer to such fund groups as operating, plant, endowment, and other funds (FAS 117, Par. 98).

permanent restriction

“A donor-imposed restriction that stipulates that resources be maintained permanently but permits the organization to use up or expend part or all of the income (or other economic benefits) derived from the donated assets” (FAS 117, Par. 168). Information about permanent restrictions is useful in determining the extent to which an organization's net assets are not a source of cash for payments to present or prospective lenders, suppliers, or employees and thus are not expected to be directly available for providing services or paying creditors (FAS 117, Par. 98).

pledges

receipts of promises to give

temporary restriction

“A donor-imposed restriction that permits the donee organization to use up or expend the donated assets as specified and is satisfied either by the passage of time or by actions of the organization” (FAS 117, Par. 168). Separate line items may be reported within temporarily restricted net assets or in notes to financial statements to distinguish between temporary restrictions for (a) support of particular operating activities, (b) investment for a specified term, (c) use in a specified future period, or (d) acquisition of long-lived assets. Donors' temporary restrictions may require that resources be used in a later period or after a specified date (time restrictions), or that resources be used for a specified purpose (purpose restrictions), or both. For example, gifts of cash and other assets with stipulations that they be invested to provide a source of income for a specified term and that the income be used for a specified purpose are both time and purpose restricted. Those gifts often are called term endowments (FAS 117, Par. 15).

Further Readings

Baber, William R., Patricia L. Daniel, and Andrea A. Roberts. 2002. “Compensation to managers of charitable organizations: An empirical study of the role of accounting measures of program activities.” Accounting Review (77, 3, July), pp. 679–693.

The Comprehensive Report of the Special Committee on Financial Reporting. American Institute of Certified Public Accountants. 1994. Improving Business Reporting—A Customer Focus. New York: AICPA.

Council of Better Business Bureaus (CBBB). 2001. Web site for the Philanthropic Advisory Service reports. Available at:http://www.bbb.org/pas/reports .

Governmental Accounting Standards Board. 1990. Service Efforts and Accomplishments Reporting: Its Time Has Come—An Overview . Washington, DC: GASB.

Guidestar. 2001. Web site that reports Form 990, Return of Organization Exempt from Income Tax, information for charities. Available at: http://www.guidestar.org .

Houle, C. O. 1989. Governing Boards: Their Nature and Nurture . (Washington, DC: Jossey-Bass and National Center for Nonprofit Boards).

Joos, Peter, and George A. Plesko. 2005. “Valuing loss firms.” Accounting Review (80, 3, July), pp. 847–870.

Laswad, Fawzi, Richard Fisher, and Peter Oyelere. 2005. “Determinants of voluntary Internet financial reporting by local government authorities.” Journal of Accounting and Public Policy (24, 2, March/April), pp. 101–121.

Parry, Robert W., Florence Sharp, Jannet Vreeland, and Wanda A. Wallace. 1994. “The role of service efforts and accomplishments reporting in total quality management: Implications for accountants.” Accounting Horizons (8, 2, June), pp. 25–43.

Peebles, Laura. 2001. “The right philanthropic vehicle.” Journal of Accountancy (July), pp. 22–27.

Ripperger, Matt. 2001. “Analyst [A director with Warburg Dillon Read's Healthcare Research Group] interview: Hospital management services.” Wall Street Journal Transcript (February 7), Document # LAQ901.

Wallace, Wanda A. 2006. “Financial management in government entails evaluating nonprofits: Are you ready for the next natural disaster?” Journal of Government Financial Management (55, 1, Spring), pp. 44–57.

Wallace, Wanda A. 2003. “Avoiding the downfall of windfalls.” Journal of Government Financial Management (52, 3, Fall), pp. 18–30.

Wallace, Wanda A. 2001. “How accountable are charities for their performance?” Accounting Today (June 18–July 1), pp. 18, 20.

Accounting deals with a system which is a human creation, designed to satisfy human needs, and which must therefore, above all, be useful. The accounting environment is prone to many influences of a nondeterministic nature, influences related not only to long-term legal, cultural and political traditions, but also to short-term movements of mass psychology…. The subject matter is of such diversity and changing complexity that attempts to make predictions in accounting are akin to the difficulties of predicting the conditions of turbulence inside a tornado or the problem of “forecasting” next month's weather.

In principle it is possible for meteorologists to predict the weather at noon in Chicago on January 1, 1981, just as it is possible in principle to predict an eclipse of the sun a thousand years hence. In practice, weather predictions (unlike astronomical predictions) are unreliable over the space of a month let alone a millennium. Accountants, like meteorologists, are also faced with a complex world of many interacting bodies. Nevertheless, they might be able to adopt the pure scientific method, and perhaps enjoy as much success with it as meteorologists, if—like—meteorologists—they only had to deal with the behavior of inhuman molecules. But in contrast, the accountant's “molecules” think and feel, they have traditions and cultures, they are governed by laws, act sometimes rationally and often irrationally, and are susceptible to an enormous variety of psychological, social, economic, cultural, and political influences…. Accountancy … deals with problems involving equity and balance and the resolution of conflict between different groups of human beings with widely varying interest and objectives.

—Edward Stamp

[Source: “Why Can Accounting Not Become a Science Like Physics?” ABACUS (Vol. 17, No. 1, 1981), p. 21]

Case 4Clarus Corporation: Recurring Revenue Recognition

Case Topics Outline

Clarus Corporation

Press Release

Analysts' Observations

The New Economy Meets Tradition

Clarus Corporation announced a change in its business strategy to support a broader range of software licensing arrangements. This meant definitionally that the company would move from the up-front license fee revenue model that had been used toward a subscription-based licensing arrangement that would require a ratable revenue recognition approach. The company understood that as a result of this change in policy, historical and future financial statement figures might not be comparable. Clarus Corporation issued a press release on December 15, 2000, excerpts from which follow:

Clarus Expands Business Strategy and Model; Clarus Announces Initiatives To Serve the Growing Large to Mid-Sized Enterprise Market

Clarus (NASDAQ:CLRS), a leading business-to-business (B2B) e-commerce solution provider, today announced its strategy to meet the growing demand in the large to mid-size enterprise (LME) market. This expansion of its market strategy is designed to accelerate adoption and results in a business model with a greater emphasis on recurring revenue.

Clarus has focused on the LME market and has established itself as a leader in B2B e-commerce solutions…. Industry experts … report the LME market is entering a period of accelerated adoption. The Clarus solutions are designed to meet the needs of this target market by offering lower cost of ownership and speed of deployment advantages. As Clarus intensifies its focus on the needs of the LME market it will leverage key strategic partners … to deliver “turnkey” packages and fixed-fee offerings.

“Global market adoption of electronic procurement solutions is less than one percent and even lower in the LME space,” said Steve Jeffery, president and CEO of Clarus. “Clarus is positioned to meet this market opportunity with the right mix of products, services, partnerships and pricing.”

Key to meeting the demand in this market will be breaking down the barriers to widespread adoption by reducing the risks and costs associated with traditional licensing and implementation of software. Clarus will move to a business model that will provide its customers greater flexibility to choose the way in which they procure their e-commerce solutions. Under this model, Clarus will recognize revenue from the sale of its products over a fixed period of time, reducing the upfront revenue recorded as compared with its traditional model, while generating an increase in the amount of sales backlog.

“This business model and strategy is an evolution of Clarus' longtime focus on the LME market,” stated Jeffery. “We believe this shift will not only allow us to drive rapid customer adoption through directly addressing the needs of this target market, but will also provide a more stable and predictable financial model.”

In order to meet the unique needs of the LME market, the majority of future Clarus contracts with customers will not meet the criteria for immediate revenue recognition. Instead, a recurring, predictable revenue stream will be recognized over an estimated 12 to 24 month period. Clarus anticipates that approximately 90 percent of its license business will be contracted under agreements requiring ratable revenue recognition.

Clarus also provided guidance for fourth quarter 2000 and for its fiscal year 2001 and 2002. Under the ratable revenue recognition model, the company expects fourth quarter 2000 revenue to be in the range of $4 million to $4.5 million, with an operating loss per share, excluding non-cash charges, of approximately $1.40. For fiscal year 2001, the company expects revenue to be in the range of $45 million to $50 million, and EPS, excluding non-cash charges, of ($2.14). Fiscal year 2002 projections are for revenues in the range of $115 million to $120 million, and EPS, excluding non-cash charges, of $1.08. The company plans to reach breakeven on a cash basis in the first quarter 2002, with profitability on a cash basis projected for the second quarter 2002….

Clarus will host an investor conference call to discuss this announcement today….

About Clarus Corp.

Atlanta-based Clarus Corporation (http://www.claruscorp.com; NASDAQ: CLRS), a leader in business-to-business (B2B) e-commerce, provides B2B procurement software and trading services that exploit the global marketplace of the Internet to manage corporate purchasing and enable digital marketplaces. … provides a comprehensive range of critical trading services such as payment settlement, supplier enablement, auctions, integration, and analytics. Designed to provide unprecedented interoperability…

THIS PRESS RELEASE CONTAINS FORWARD-LOOKING STATEMENTS WITHIN THE MEANING OF SECTION 27A OF THE SECURITIES ACT OF 1933 AND SECTION 21E OF THE EXCHANGE ACT. ACTUAL RESULTS COULD DIFFER MATERIALLY FROM THOSE PROJECTED IN THE FORWARD-LOOKING STATEMENTS AS A RESULT OF CERTAIN RISKS INCLUDING THAT THE BENEFITS EXPECTED BY THE COMPANY AS A RESULT OF THIS ANNOUNCEMENT MAY NOT OCCUR…. (Source: Press Release on 12/15/2000)

Analysts describe Clarus as a company providing e-business solutions that enable procurement, supply-chain management, customer-and-supplier relationship management, and demand management processes of various enterprises—citing such competitors as Global Sources, Commerce One, FreeMarkets, and Ariba. In evaluating Clarus, the analysts compare a trading price in mid-2001 around $6 as low relative to a so-called cash per share value estimate from $7 to $10. The analysts point out that revenue growth is not evidenced in the financial statements because of a change in revenue recognition from what they refer to as a traditional license model and an up-front license model, toward a recurring revenue recognition model. As a result, quarter-to-quarter revenue comparisons witness a large decline from September to December. An interesting point is that the increased backlogs are essentially sources of future revenue.

In its annual filing with the SEC, Clarus Corporation described its revenue stream and relevant accounting principles as follows:

Sources of Revenue

The Company's revenue consists of license fees and services fees. License fees are generated from the licensing of the Company's suite of products. Services fees are generated from consulting, implementation, training, content aggregation and maintenance support services.

Revenue Recognition

The Company recognizes revenue from two primary sources, software licenses and services. Revenue from software licensing and services fees is recognized in accordance with Statement of Position (“SOP”) 97-2, “Software Revenue Recognition”, and SOP 98-9, “Software Revenue Recognition with Respect to Certain Transactions”. Accordingly, the Company recognizes software license revenue when: (1) persuasive evidence of an arrangement exists; (2) delivery has occurred; (3) the fee is fixed or determinable; and (4) collectibility is probable.

SOP No. 97-2 generally requires revenue earned on software arrangements involving multiple elements to be allocated to each element based on the relative fair values of the elements. The fair value of an element must be based on evidence that is specific to the vendor. License fee revenue allocated to software products generally is recognized upon delivery of the products or deferred and recognized in future periods to the extent that an arrangement includes one or more elements to be delivered at a future date and for which fair values have not been established. Revenue allocated to maintenance is recognized ratably over the maintenance term, which is typically 12 months and revenue allocated to training and other service elements is recognized as the services are performed.

Under SOP No. 98-9, if evidence of fair value does not exist for all elements of a license agreement and post-contract customer support is the only undelivered element, then all revenue for the license arrangement is recognized ratably over the term of the agreement as license revenue. If evidence of fair value of all undelivered elements exists but evidence does not exist for one or more delivered elements, then revenue is recognized using the residual method. Under the residual method, the fair value of the undelivered elements is deferred and the remaining portion of the arrangement fee is recognized as revenue. Revenue from hosted software agreements are recognized ratably over the term of the hosting arrangements. (Source: 10-K filed on 3/21/2001)

Requirement A: Comparing Revenue Recognition Approaches

Clarus Corporation's 1999 and 2000 data divided between its previous human resources and financial software business (ERP) and the current e-commerce business, along with a few other pieces of financial information are reported in Table 5.4-1.

How does the described revenue recognition approach compare to other industry settings?

The analysts' reference to traditional license models in B2B (business-to-business) relate to up-front models in the “new economy,” yet some would argue that tradition in accounting defers revenue to match the earnings process over time. In what sense has the new economy met tradition in the Clarus Company example? Explain, with support from FARS.

Do you concur that the recurring revenue recognition will enhance both visibility and predictability of financial results? Why or why not? (Hint: Access the Staff Accounting Bulletin (SAB) 101 on Revenue Recognition athttp://www.sec.gov/interps/account/sab101.htm.)

Table 5.4-1. Financial Information

| Clarus Corporation Results of Operations * (in thousands) | Year Ended December 31, 2000 | Year Ended December 31, 1999 |

| Revenues: e-commerce |

|

|

| License fees | $24,686 | $9,969 |

| Services fees | 9,361 | 1,515 |

| Total revenues development | 34,047 | 11,484 |

| Revenues: ERP |

|

|

| License fees | 5,132 | |

| Services fees | 21,526 | |

| Total revenues | 26,658 | |

| Cost of revenues: e-commerce |

|

|

| License fees | 154 | 400 |

| Services fees | 12,776 | 3,130 |

| Total cost of revenues | 12,930 | 3,530 |

| Cost of revenues: ERP |

|

|

| License fees | 951 | |

| Services fees | 11,387 | |

| Total cost of revenues | 12,338 | |

| Total operating expenses | 98,455 | 37,429 |

| Operating loss | (77,338) | (15,155) |

* Source: 10-K filing on 3/21/2001.

Requirement B: Strategy-Related Considerations

Clarus Corporation accords attention to the fact that in October 1999, the Company sold its ERP business. Are there added complications of such an event for the evaluator of the company's financial performance? Explain.

Hindsight

Access Clarus Corporation's 10-Q for the quarterly period ended June 30, 2006 from http://sec.gov. Explain what has happened to the company subsequent to 2000. What is particularly unique about the income statement? Access the 10-K for the fiscal year ended December 31, 2005 to augment the information from the 10-Q and describe the entity's strategy going forward.

Directed Self-Study

Does Statement of Financial Accounting Standards No. 152 change revenue recognition practices in any manner? Use FARS to explore this question. [Access FASB-OP (amended), click on the Search toolbar, select the option Search Within a Single OP Document Title, type fas 152 into the document title box and in the Query For: box type revenue recognition.]

revenue recognition

when revenue is recorded: revenue must be earned and realized or realizable before being recognized—two key criteria for recognition: (1) what constitutes substantive performance by a vendor [i.e., when is the earnings process substantially complete—SFAC No. 5, par. 83(b)]? and (2) how much assurance of collectibility is needed to justify recognition of revenue [i.e., when is revenue realized or realizable]?

subscription revenue

an example might be revenues for a newspaper, which tend to be recorded as earned, pro rata, on a monthly basis, over the life of the subscriptions

“turnkey” packages

reference to off-the-shelf product as distinguished from tailor-made software; the idea is to just “turn the key” to start the ready-made, standardized software

Further Readings

Altamuro, Jennifer, Anne L. Beatty, and Joseph Weber, 2005. “The effects of accelerated revenue recognition on earnings management and earnings informativeness: Evidence from SEC Staff Accounting Bulletin No. 101.” The Accounting Review (80, 2, April), pp. 373–401.

Beaver, William H. 2002. “Perspectives on recent capital market research.” Accounting Review (77, 2, April), pp. 453–474.

Berenson, Alex. 2001. “A software company runs out of tricks.” New York Times (April 29).

Berenson, Alex. 2001. “Computer Associates officials defend accounting methods.” New York Times Company (May 1).

Bonner, S. E., Z. Palmrose, and S. M. Young. 1998. “Fraud type and auditor litigation: An analysis of SEC accounting and auditing enforcement releases.” Accounting Review (73, 4), pp. 503–532.

Bushee Brian J. , Dawn A. Matsumoto, and Gregory S. Miller. 2004. “Managerial and investor responses to disclosure regulation: The case of reg FD and conference calls.” Accounting Review (79, 3, July), pp. 617–643.

Davis, Angela K. 2002. “The value relevance of revenue for Internet firms: Does reporting grossed-up and barter revenue make a difference?” Journal of Accounting Research (40, 2), pp. 445–477.

Davis, A.K., R. Bowen, and S. Rajgopal. 2002. “Determinants of revenue recognition policies for Internet firms.” Contemporary Accounting Research (19, 4), pp. 523–562.

Feroz, E. H., K. Park, and V. S. Pastena. 1991. “The financial and market effects of the SEC's accounting and auditing enforcement releases.” Journal of Accounting Research (29, Supplement), pp. 107–142.

Guidera, Jerry. 2001. “Computer Associates posts quarterly loss of $410 million.” Wall Street Journal (May 23), p. B6.

Henry, David. 2001. “The numbers game.” Business Week (May 14), pp. 100–110.

Hudack, Lawrence R., and John P. McAllister. 1994. “An investigation of the FASB's application of its decision usefulness criteria.”Accounting Horizons (8, 3), pp. 1–18.

Kimbrough, Michael D. 2005. “The effect of conference calls on analyst and market underreaction to earnings announcements.”The Accounting Review (80, 1), pp. 189–219.

McNamee, David, and Sally Chan. 2001. “Under- standing e-commerce risk.” Internal Auditor (April), pp. 60–61.

Ness Joseph A. , Michael J. Schroeck, Rick A. Letendre, and Willmar J. Doublas. 2001. “The role of ABM in measuring customer value, part one.” Strategic Finance (March), pp. 32–37.

“News report: Financial reporting—Online financial reports show problems and promise.” 2000. Journal of Accountancy (189, 2, February).

OECD Convention on Combating Bribery of Foreign Public Officials. 2000. “Financial transparency and accountability initiative: Overall observations” (April 17). Available at: http://www.transparency-usa.org .

Philipich, Kirk L., Michael L. Costigan, and Linda M. Lovata. 1994. “The corroborative relation between earnings and cash flow information.” Advances in Accounting 12, pp. 31–50.

Phillips, Jr., Thomas J., Michael S. Luehlfing, Cynthia M. Daily. 2001. “Financial reporting/auditing—The right way to recognize revenue.” Journal of Accountancy (191, 6, June).

Price, Jimmy. 2001. “Auditing e-business applications.” Internal Auditor (August), pp. 21–23.

Schuetze, Walter P. 2005. “Statements of quality [editorial commentary].” Barron's (May 30), p. 39.

SEC. 2003. “Frequently asked questions regarding the use of non-GAAP financial measures.” Prepared by staff members in the Division of Corporation Finance. Washington, DC: U.S. SEC (June 13).

SEC. 1999. “SEC Staff Accounting Bulletin (SAB): No. 101—Revenue Recognition in Financial Statements. 17 CFR Part 211.

Shridharani, Kaushik. 2001. “E-business applications.” Analyst interview (CFA and Managing Director in equity research with Bear, Stearns & Co.). Wall Street Journal transcript (May 21).

“Special report, professional issues—COSO's new fraud study: What it means for CPAs.” 1999. Journal of Accountancy (187, 5, May). [The Institute's Web site ( http://www.aicpa.org ) has an executive summary of the study.]

Thurm, Scott and Jonathan Weil. 2001. “Money & investing: Tech companies charge now, may profit later.” Wall Street Journal(April 27).

Tie, Robert. 2001. “E-commerce: Get ready for the world of B2B.” Journal of Accountancy (191, 6, June).

UBS Investment Research, Global Analyzer. 2003. S&P 500 Accounting Quality Monitor, Bridging the Gap to GAAP EPS (July 2), pp. 1–120.

Wallace, Wanda A. 2002. Pro Forma Before and After the SEC's Warning: A Quantification of Reporting Variances from GAAP . (Morristown, NJ: Financial Executives International (FEI) Research Foundation) (March): ISBN 1-885065-33-7.

Wallace, Wanda A. 2001. “EBITDA: Freedom of speech or freedom to confuse?” Accounting Today (15, 7, April 16–May 6), pp. 34, 35, 45.

Zarowin, Stanley. 2001. “Facing the future.” Journal of Accountancy (April), pp. 26–31.