Good day, I would love to get assistance with my assignment.

HSA 312 XT81/H01/01

MANAGED HEALTH CARE

SPRING 2020 L. EITEL

READING 1.C.

THE CRISIS OF THE PREVAILING EMPLOYER-BASED INDEMNITY/SERVICE PLAN, THE MASSIVE SHIFT TO MANAGED HEALTH CARE PLANS 1988-1996, AND THE MANAGED CARE BACKLASH

HEALTH INSURANCE IN THE UNITED STATES: CRISIS AND TRANSITION – LATE 1960s THROUGH EARLY 1990s

CHALLENGES TO THE SUSTAINABILITY OF THE EMPLOYER-BASED GROUP HEALTH INSURANCE MODEL FROM THE 1960’S THROUGH THE EARLY 1970S.

The influx of Medicare and Medicaid recipients making demands on the U.S. Health Care services system beginning in the late 1960s interacted in a variety of complicated ways with other changes going on in that system to produce substantive and unprecedented increases in the portion of Gross Domestic Product allocated to health care services, and in sustained year-to-year increases in National Health Expenditures.

These substantive increases in price and expenditure started to threaten the stability of the prevailing system of Indemnity and Service health insurance plans – would premiums become unaffordable for workers and their employers? How would that impact on the accessibility and affordability of health insurance for a large percentage of the American population?

For Details: See Reading 3 in the Required Readings for February 18, 20, and 24.

Managed Care and HMOs began to be seen by some politicians, policy makers, academicians, and advocates of the primacy of Primary Care as a quality-oriented answer to the prevailing health insurance system’s inability to address massive, sustained price and expenditure increases. President Nixon and Congress in 1973 approved the HMO Act of 1973, which played a major role in the 1970s and 1980s in starting the spread of Managed Care Health plans beyond their East and West Coast strongholds and breaking down local resistance to the previously marginalized Managed Care health insurance plans.

II. THE MASS MOVEMENT OF AMERICANS WITH EMPLOYER-BASED GROUP HEALTH INSURANCE FROM INDEMNITY AND SERVICE PLANS TO MANAGED CARE HEALTH PLANS 1988 - 1996.

Throughout the late 1970s through the 1980s, Blue Cross and Blue Shield health insurers, and large commercial health insurers, tried to maintain and save the Indemnity and Service plans in which the vast majority of Americans with employer-based insurance were enrolled.

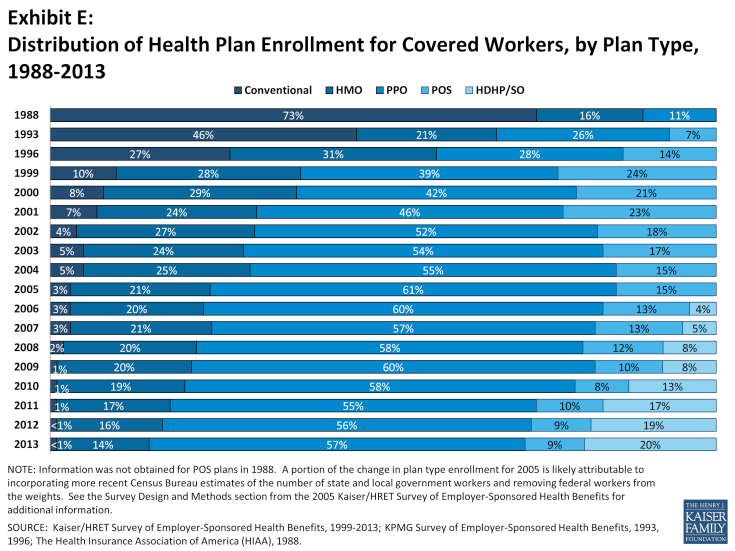

(As late as 1988 73% of American workers and their families who were covered by employer-based private group health insurance were enrolled in those Indemnity and Service plans.)

Indemnity and Service Plans had originally been thoroughly opposed to the idea and practice of Managed Care (as exemplified in the Kaiser-Permanente Model). These plans followed the principles of non-interference in the practice of medicine, unrestricted consumer choice of a health care service provider, and non-interference in the decisions of patients and physicians about the preferred place of and treatment for a given medical condition.

In part inspired by Federal government experiments in Utilization Review and Management, these plans started to adopt some aspects of Managed Health Plan/HMO practice in order to constrain annual expenditure increases for Personal Health Care Services. They adopted Large Case Management programs, Utilization Review programs, and used other medical management tools traditionally uses by Managed Health Insurance plans, and thus started to do just what physicians and hospitals had feared prior to 1930 – they started to involve themselves in decisions of length of treatment, type of treatment, appropriateness of treatment, and place of treatment for some health insurance plan members.

These changes in health insurance plan management and philosophy did not have a significant impact on health expenditures, and were not likely to keep premiums and out-of-pocket expenditures from increasing substantially. These changes did not significantly impact rapidly rising prices of health care goods and services, nor did they affect the significant year-to-year increases in national health expenditures and health insurance premiums.

Faced with the likelihood of severely disappointing employers and employees by substantially increasing premiums and out-of-pocket expenditures, and reducing benefits covered by the Indemnity and Service Plans, the major insurers faced a collapse in the health insurance system which had prevailed since the 1930’s, with a resulting threat to the welfare of employees and the viability of the private group health insurance industry.

Blue Cross and Blue Shield health insurance plans, all the plans managed by commercial insurers, and the newer insurance companies which focused more heavily on providing Managed Health Insurance Plans, worked with employers to transition most Americans with employer-based health insurance to Managed Health Insurance Plans between 1988 and 1996. It was believed that only Managed Health Insurance Plans would allow those companies to continue offering generous packages of health insurance benefits, and would enable them to control the growth in personal health care expenditures, prices, and the volume of services produced. The price of maintaining the private group health insurance industry’s viability would be the wholesale movement of employer-based group health insurance enrollees to Managed Health Insurance Plans.

Between 1988 and 1996 the relative significance of Indemnity/Service Plans and Managed Care Plans in the lives of American employees and their families was reversed. By 1996 73% of American workers with employer-based group health insurance were enrolled in those Managed Health Insurance Plans. By 2000 92% of those workers and their families were in Managed Health Insurance Plans – HMOs, Point of Service Plans, and Preferred Provider Organizations.

This massive change in the type of health insurance most Americans relied upon to ensure their access to affordable health care services was dramatic and for many Americans a shock. Previously, access to acute care services, diagnostic services, specialty services including consultations, and the full array of personal health care services involved minimal interference from the health insurance plans. Now most Americans would face limits on that access, especially in the form of having to access most services with approval either from an assigned Primary Care Practitioner, or from medical management personnel associated with the respective insurance plans.

IV. THE PHILOSOPHY OF MANAGED CARE – A FOCUS ON CONTINUOUS, COMPREHENSIVE, COORDINATED HEALTH CARE FOR INSURANCE PLAN ENROLLEES:

READINGS 4.A., 4.B., 4.C. – REQUIRED READINGS AND CRITICAL STUDY QUESTIONS FOR FEBRUARY 18, 20, 24.

Kaiser Permanente’s philosophy of Managed Care, which focuses on the primacy of Primary Care and the necessity for highly coordinated efforts by insurers and providers, was a major inspiration for the types of Managed Health Insurance Plans implemented throughout the 1990s.

Essential to the Kaiser Permanente philosophy was the belief in the primacy of Primary Care within the system by which personal health care services were delivered in the United states. This belief, championed from the 1960’s and thereafter by policy makers such as Barbara Starfield, asserted that reasonably priced quality health care could only be delivered on a routine basis if patients worked closely and routinely with assigned Primary Care Physicians (individuals and/or teams).

At the heart of this belief in the centrality and primacy of Primary Care was a belief that Primary Care Practitioners were best equipped to ensure that patients and their families received Continuous, Comprehensive, and Coordinated patient care.

V. THE PRINCIPAL TYPES OF MANAGED CARE PLANS IMPLEMENTED IN THE 1990s – HEALTH MAINTENANCE ORGANIZATIONS (HMOs), POINT OF SERVICE PLANS (POS), AND PREFERRED PROVIDER ORGANIZATIONS (PPO).

By the late 1980s the primary kinds of Managed Care Health Plans had been developed, and were offered to employers and employees throughout the period of the great health insurance plan transitions between 1988 and 1996.

HMOs, Point of Service Plans, and PPOs varied in the extent to which the particular type of insurance plan regulated key aspects of the process by which enrollees, advised by doctors, accessed personal health care services covered by those plans.

Key areas in which Managed Care Plans differed in the intensity and extent of their control of medical management, and physician and plan enrollee choice, included the following:

Managing limited networks of individual and institutional providers, and requiring that plan enrollees only used those provider networks to access care.

Requiring plan enrollees and their families to access most personal health care services with the approval of a “gatekeeper” or Primary Care Practitioner (individual or team.)

Aggressively negotiating payment rates for provider services, often using capitation for Primary Care Practitioners, and negotiating lower payment rates for Specialty Care Practitioners.

Requiring PCPs to take on extensive risk.

Implementing extensive Utilization Management, Case Management, and Disease Management programs.

Subjecting critical decisions on selected hospital admissions, access to diagnostic imaging, and access to specialty physician consultations to approval not only from PCPs, but from medical management staff within the plan.

HMOs and POS plans were most controlling forms of Managed Health Insurance, and PPOs were much less so.

In the 1990s HMOs and POS plans had the highest levels of enrollment, unlike the post Managed Care Backlash experience in the post- 2000 era when PPOs predominated (and continue to do so).

Understanding the various types of Managed Care Health Insurance Plans, their relative levels of enrollment, and the different ways they impacted on providers, employers, and plan enrollees in the 1990s is key to understanding the successes and failures of these plans in the 1990s, and understanding the Managed Care Backlash.

6