Waiting for answer This question has not been answered yet. You can hire a professional tutor to get the answer.

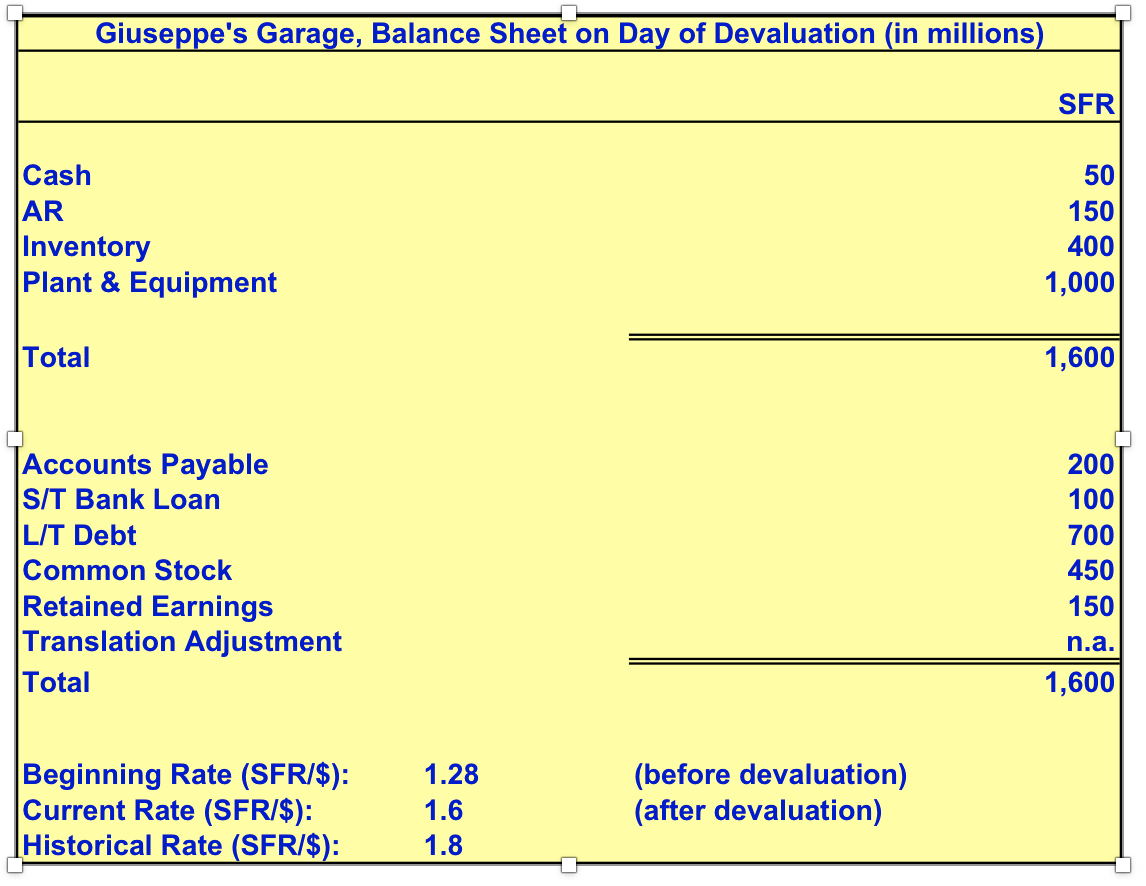

Giuse - ne's Gara- e, Balance Shee on Da of Devaluation in millions Cash AR Inventory Plant amp;amp; Equipment Total Accounts Payable SIT Bank Loan...

The last time the Swiss balance sheet was translated, the exchange rate was SFR1.28/$. Today the franc was devalued by 20% so that current exchange rate is SFR1.60/$.

a.If Giuseppe's functional currency is the Swiss franc, show the translated dollar value for both pre- and post-devaluation scenarios. What is the translation gain (loss) due to the devaluation? (Note, for translated amounts before the devaluation, use a "plug" figure for Retained Earnings and assume that there weren't any previous translation losses).

b.If Giuseppe's functional currency is the US dollar, show the translated dollar value for both pre- and post-devaluation scenarios. What is the translation gain (loss) due to the devaluation? (Note, for translated amounts before the devaluation, use a "plug" figure for Retained Earnings.)

2.Lotus, a British automobile manufacturer, has contracted to buy engines from Toyota worth ¥33 billion. The invoice for the engines is payable in three months. Lotus also has receivables for cars sold to Marubeni, its Japanese dealer; these receivables are valued at ¥21 billion, also due in three months. Lotus' policy is to hedge all residual currency positions. Disregard transaction costs and assume that the current spot exchange rates is £1 = ¥225 and the three-month forward rate is £1 = ¥223. Interest rates in the United Kingdom and Japan are 12.8 percent per annum and 6.0 percent per annum, respectively (assume that borrowing and lending rates are the same). Also, three month calls and put with a strike price of £1 = ¥223 are available at a premium of 1.5%.

a.How can Lotus undertake an effective hedge in the forward market?

b.How can Lotus undertake an effective money market hedge?

c.Suppose Lotus' FX manager believes that the actual spot rate in three months will likely be £1 = ¥224. Would Lotus be better off being unhedged rather than using the forward or money market hedges? If yes, what would be its savings?

d.However, even though she is confident in her forecasts, to protect against any downside risk, the manager buys the appropriate options contract. What kind of options would she buy today and how much in premium would she have to pay? If her forecast turns out to be right, what is the net cost of the transaction to Lotus in managing the exposure with options contracts?

{kind=link}