Waiting for answer This question has not been answered yet. You can hire a professional tutor to get the answer.

MASTER FINANCE

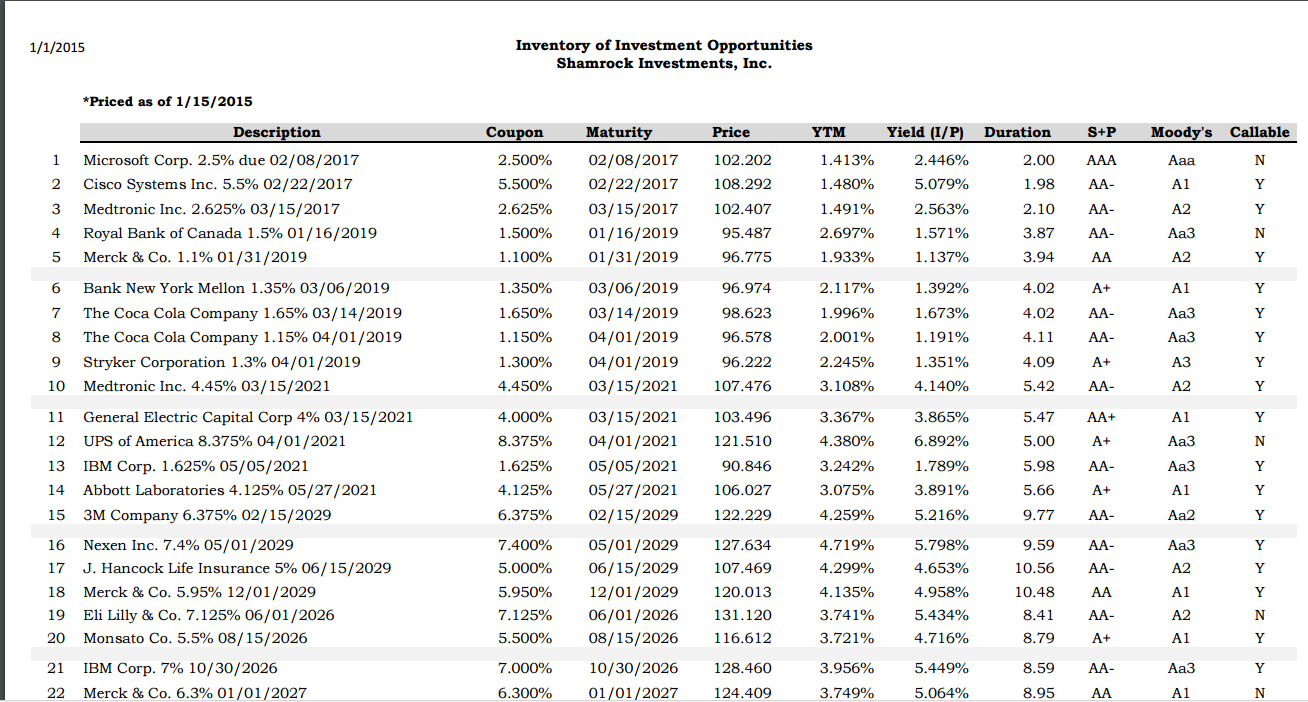

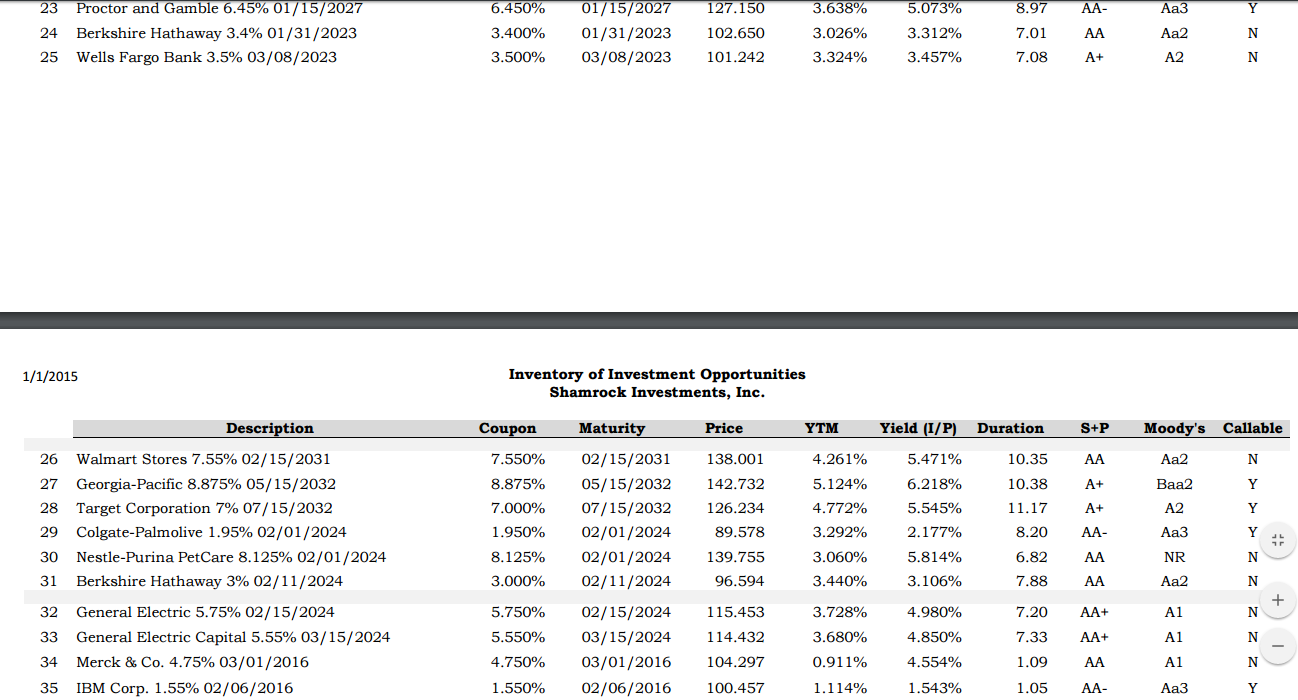

You are a bond portfolio manager and are given $10 million US dollars by a client to be invested entirely in Fixed Income. The client desires a yield on the portfolio equal to the benchmark’s yield plus 100 bp. The client also requires that a maximum allocation to high yield or junk bonds be 20% of the portfolio. The money belongs to part of a qualified trust and hence is non-taxable. Your firm actively manages duration in order to take advantage of directional volatility, anticipated changes to the shape of the yield curve, and also to prevent loss of principal. Your firm does not maintain cash balances and the client does not require liquidity for withdrawals or other expenses. The the client expects to make withdrawals in approximately fifteen years. Attached is a spreadsheet with twenty issues with various characteristics. It is the inventory of a sell-side firm your firm does business with.

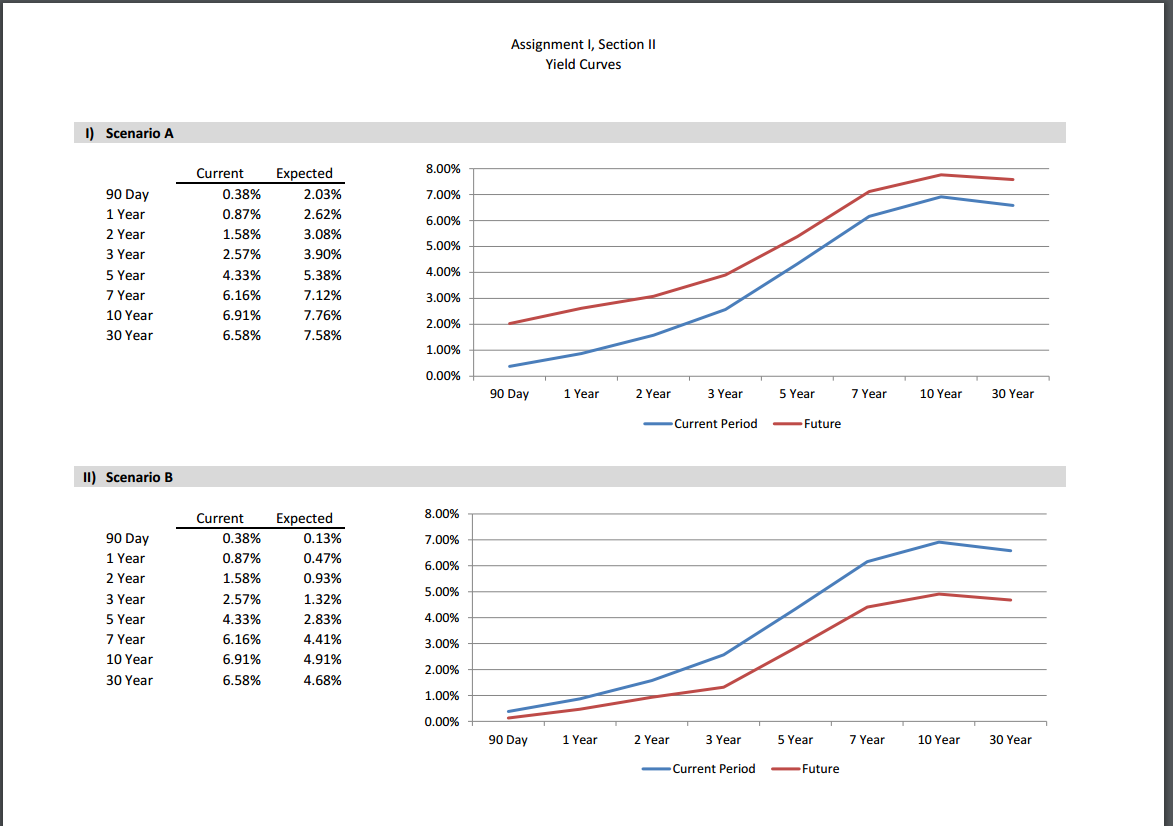

1) Given an expected flattening twist (upward) in market rates, where the short-end of the Yield Curve increases by 175 bp and the long end by 85 bp, construct a portfolio appropriate for this scenario but also provides the yield desired by the client. The scenario is displayed in Yield Curve A. a. Why did you choose the issues you choose? b. Given your selected holdings, what will the change in portfolio value be? c. What is the total value? d. What is the portfolio’s yield?

2) Given an expected downward (steepening) in market rates, where the short-end decreases by 125 bp and the long-end by 200 bp, construct a portfolio appropriate for this scenario but also provides the yield desired by the client. The scenario is displayed in Yield Curve B. a. Why did you choose the issues you choose? b. Given your selected holdings, what will the change in portfolio value be? c. What is the total value? d. What is the portfolio’s yield?

{kind=link}

{kind=link}

{kind=link}

{kind=link}