Waiting for answer This question has not been answered yet. You can hire a professional tutor to get the answer.

QUESTION

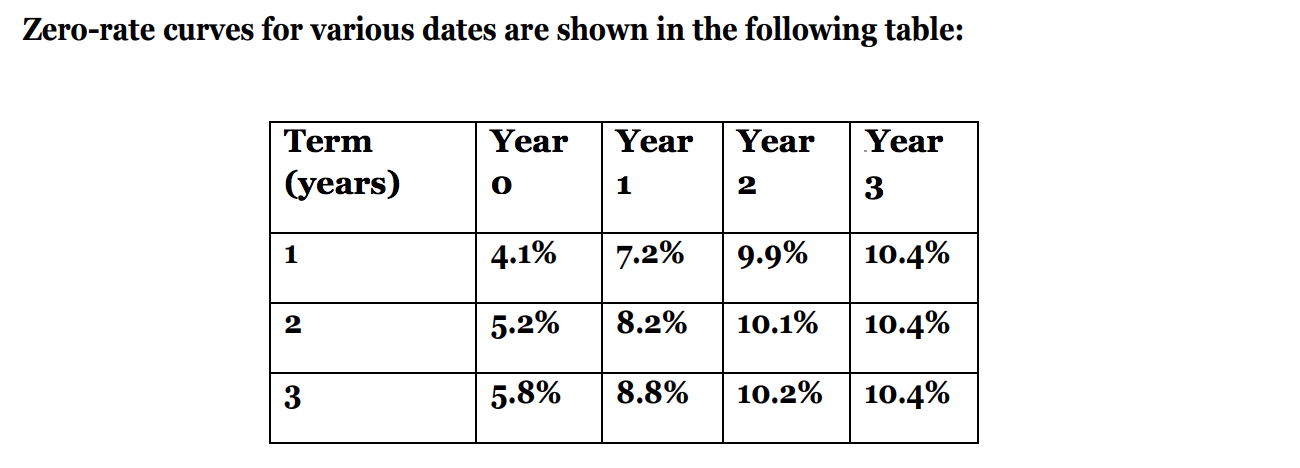

Zero-rate curves for various dates are shown in the following table: Year ear Year .Y ear 0 2 3 5.2% 10.8% 10.2% 10.

How do you calculate the price (per $100 par value) of a default-free bond with annual coupon rate of 5% and exactly 3 years to maturity? Does the bond trade at par, at premium or discount? Would you expect the bond's yield to be equal to, greater or less than the coupon rate?

{kind=link}