Answered You can hire a professional tutor to get the answer.

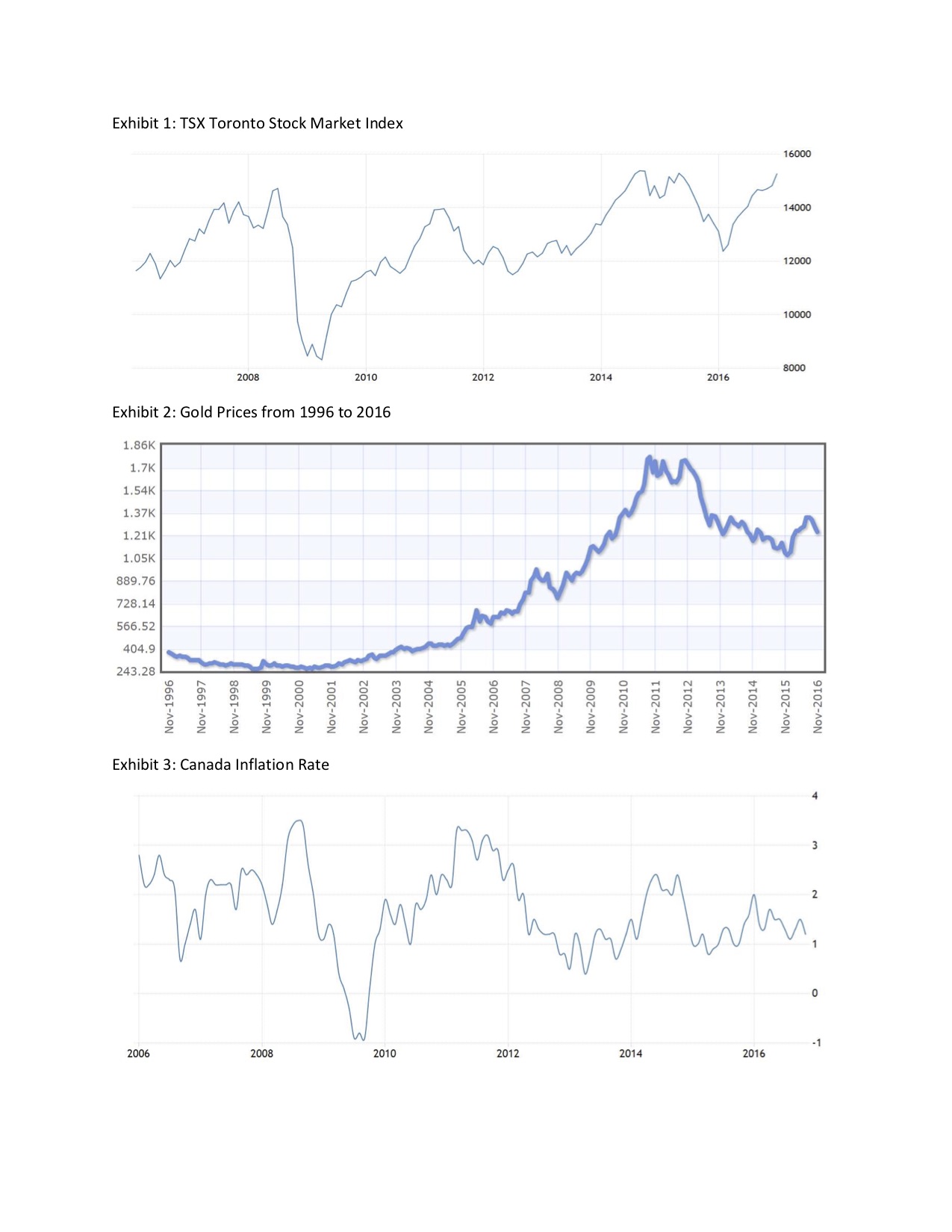

Exhibit 1: TSX Toronto Stock Market Index 15000 140m 120m 100m 2016 2014 201 2. 2010 2000 Exhibit 2: Gold Prices from 1996 to 2016 1.86K 1.7K 1.54K

Alamo Gold

You are the CFO of Alamo Gold. You just finished reviewing a preliminary acquisition for an exciting new opportunity to expand Alamo's mining capacity by acquiring a new mine near Yukon Territory. This acquisition would significantly increase Alamo's verified mineable reserves, and position it as an important player in the gold export market. However, before doing so, you need to ensure that this investment will create value for your firm. You need the green light from the board and convince your banker to provide the necessary financing.

Company Background

Alamo Gold was established in 1905 to conduct gold mining business in Canada. It owns three mines, mainly in the surrounding areas of Alberta and Yukon Territory, with a combined 7 hectares of gold mining concession area and an estimated 40 tons of gold reserves. It produced approximately 2 tons of gold per year. The company operates under strict guidelines, conforming to all health and environmental safety standards. It aims to continuously improve via quality management systems, minimizing occupational hazards and environmental impact, and saving energy and other resources. Its gold production was mainly sold to domestic and international companies.

Since its incorporation, the company has enjoyed financial success with operating margins and return on invested capital averaging 21% and 16% in the last five years. As seen in Exhibit 4, its sales volume (in tons) increased every year from 2012 - 2016, even though revenue experienced a decline in due to the decline in gold prices. Compared to other companies in the industry, illustrated in Exhibit 6, Alamo was a very small player. However, its operating margin in 2016 was better than most. The debt-to-equity ratios for the industry players vary widely.

The Gold Industry

While gold-mining companies in Canada have generally fared well, the risks, especially to small miners, is not insignificant. The decline in gold prices in the last few years resulted in the closure of some small producers in Canada. This put additional pressure on miners, especially those who used debt extensively. These companies were hoping to cope with declining margins by producing more to recover the cost of their infrastructure, but the declining margins make this difficult.

The Investment Proposal

The proposed price of the mine is reasonable. The verifiable reserves of ore are estimated at 12 tons. The research shows that you can easily produce at least one ton from this mine per year. The capital expenditure needed to get production started would be about US$30 million, with US$15 million outlay immediately after the deal was closed, and another US$15 million a year after. The working capital investment was estimated to be an additional $2.5 million a year starting in 2017. Besides capital costs, there were also gold-mining expenses including employee-related costs, internal and external gold transportation costs, blasting, drilling, and other mining-related costs. Additionally, there were expenses related waste disposal. The finance manager estimated that operating expenses would total US$25 per kg, and would increase at a rate of 5% per year.

To determine if the investment would create value for the firm, the finance manager needed to first estimate the weighted cost of capital (WACC) for this investment. WACC is calculated by weighting cost of debt and cost of equity, with the proportion of capital in debt (D/(D+E)) and the proportion of capital in equity (E/(D+E)), respectively.

WACC = {(D/(D+E)) x (1-T) x rD } + {(E/(E+D)) x rE} ,

where rD = cost of debt, rE = cost of equity, D = value of debt, E = value of equity, T = corporate tax rate

The finance manager figured he could get the bank to finance $12 million of the capital cost with a 10-year term loan at 14% annual interest rate, completely drawn down in 2017. The other $18 million plus $2.5 million working capital investment would come from cash in hand and equity injection from the parent firm. To estimate the cost of equity, also called the required rate of return for the owners, the finance manager believed the best way was to use the Capital Asset Pricing Model (CAPM). CAPM stipulates that the required rate of return for the equity holders for this investment varies in direct proportion with the systematic risk called beta (B).

rE = cost of equity, Rf= current government benchmark interest rate, B= beta of the investment, Rm - Rf= equity risk premium

The beta for gold mining companies was estimated to be 1.4, and the equity risk premium for projects in Canada was 8.8%. The most recent government benchmark interest rate was 7.5%. The Canadian stock market performance, the gold price and the Canadian inflation rates, and benchmark interest rates are shown in Exhibits 1, 2, 3, and 5 respectively. The finance manager also prepared the cash flow forecasts for this investment based on the prevailing Canada corporate tax rate of 25%, shown in Exhibit 7.

Your Assignment

How attractive was this investment? With the recent gold prices dropped to a level lower than those during the global financial crisis, do you think it is a good time to pursue expansion of gold mining? Will you get the green light from the board of directors to pursue the project? Would the bankers grant the $12 million term loan for this acquisition?

[The answers should include a thoughtful quantitative analysis of the case details. A good case write-up will have detailed supporting evidence such as (a) estimated free cash flows (FCF); (b) weighted average cost of capital (WACC) and (c) a thoughtful discussion of the details of the case based on your quantitative analysis. Good arguments will be supported with good facts, logic and analysis. Simply restating case facts like "the company's revenues were $118 million" is not of helpful. By the same token, just throwing out an answer such as "I believe the company is worth $10 million" is of little use without first describing how you calculated the value and explaining why the assumptions that you made are reasonable. The case provides you with a way for you to express the tools you learn in class: DCF, TVM, NPV, IRR, PI and so on. A strong case discussion will also list (d) the benefits and risks of making the investment and will conclude with a careful weighing of those considerations. The best write-ups will also include a sensitivity analysis which consider a different set of assumptions from whatever base case you are modeling and a discussion on what assumptions drive your result.]

{kind=link}